Business: The Forward Commitment

The Diagnostic Dozen: A Framework for Reading the Macro Cycle (6 of 12)

Business investment is the most honest macro signal. Consumers spend out of habit. Governments spend out of inertia. Businesses spend out of conviction. When a CEO signs a purchase order for $50 million in equipment, that is not sentiment. That is a bet on demand six to eighteen months from now, backed by real capital. When those orders stop, the bet has changed.

This is what makes the business pillar different from everything else in the framework. Surveys capture intentions. Orders capture commitments. Inventories capture mistakes. The sequencing matters: confidence turns first, then orders, then production, then inventories, then employment. By the time layoffs hit the headlines, the business cycle already turned months ago. You were just reading it wrong.

The current picture is genuinely conflicted. ISM Manufacturing just printed 52.6, breaking back into expansion for the first time in 12 months. Core capital goods orders are running at +5.9% year-over-year. Corporate profits are growing at +4.3%, modestly positive but nothing like the acceleration you’d expect if this were a new upcycle. The Leading Economic Index is still declining. Capacity utilization sits at 75.5%, well below the threshold that generates pricing power. Manufacturing is expanding output without adding workers, the leading indicators have not confirmed the turn, and regional surveys are barely above zero. The ISM says one thing. Everything else says: not so fast.

The question is whether we’re watching a genuine manufacturing stabilization or a head-fake powered by pre-tariff front-loading and fiscal impulse that fades once the orders are filled. Answering that requires looking beneath the headlines, at the subcomponents, the credit channel, and the relationship between what businesses are ordering and what they’re actually earning. That’s the framework.

The Core Insight: The Business Transmission Chain

Business activity operates through a cascading sequence: CEO Confidence leads to Capex Plans, which become Equipment Orders, which drive Production Schedules, which shape Inventory Decisions, which determine Hiring Plans, which generate Payroll Expansion, which becomes Consumer Income, which creates Final Demand, which reinforces (or undermines) CEO Confidence. A self-reinforcing loop, in both directions.

Each link has a measurable lag. Equipment orders lead GDP by 3-6 months. Hiring follows production plans by 2-4 months. Capacity utilization determines pricing power with a 3-6 month delay. Get the business call right, and you’ve captured the GDP growth rate half a year forward.

Business investment is the most cyclical GDP component. First to fall in recessions, first to rise in recoveries. One dollar of equipment spending generates income for the supplier, who hires workers, who spend wages, who create demand for other businesses. The same mechanism works in reverse.

What to Watch and Why

We organize business analysis through three lenses: surveys and sentiment (what businesses intend to do), hard data (what they actually did), and structural health (whether the foundations support continued expansion or are quietly eroding). No single indicator tells the full story. The discipline is triangulating across all three and watching for divergences.

Surveys lead because intentions precede actions. ISM surveys and Regional Fed indices give you a 2-4 week head start on the hard data. Hard data (orders, production, shipments) confirm or deny what the surveys suggested. Structural health (profits, productivity, credit conditions) tells you whether the current trend is sustainable or running on fumes.

When surveys are strong, hard data confirms, and structural health is solid, the expansion is real. When surveys are strong but employment doesn’t follow, regional breadth is weak, and the LEI hasn’t confirmed, you’re watching an expansion without conviction. That’s exactly where we are now.

The Indicators That Matter

ISM Manufacturing PMI: The Headline

The ISM Manufacturing PMI is the single most-watched business survey on the planet. Published on the first business day of each month, it gives you a read on the goods economy before any other hard data arrives. Above 50 means manufacturing is expanding. Below 50 means it is contracting. Below 45 has preceded every recession since the 1950s.

Manufacturing just broke back into expansion, printing 52.6 in January 2026. The context matters: this ends 12 consecutive months of contraction, which itself followed a brief two-month expansion that interrupted the prior 26-month contraction streak. Manufacturing has spent the better part of three years below 50. The return above it deserves attention, but it also deserves skepticism.

Why skepticism? Because the composition matters more than the headline. A PMI above 50 driven by new orders rebuilding is genuinely bullish. A PMI above 50 driven by prices surging while employment contracts is inflationary, not expansionary. The subcomponents tell you which story you’re living in.

The Mfg-Services Bifurcation: Late-Cycle Divergence

One of the most reliable late-cycle signals is when manufacturing and services diverge. Manufacturing leads because it produces physical goods that require inventory decisions, supply chain commitments, and capital investment. Services are stickier, sustained by employment contracts, subscriptions, and healthcare obligations that don’t get cancelled as quickly.

The gap is narrowing. Manufacturing PMI at 52.6 and the ISM Services composite at 53.8 puts the spread at just 1.2 points in services’ favor, down from double-digit gaps during the extreme bifurcation of 2022-2024. (The chart above uses Services Business Activity at 57.4 rather than the composite, because the composite is not available in our data feed. The composite averages Business Activity, New Orders, Employment, and Supplier Deliveries.) In the typical late-cycle sequence, manufacturing leads down first and services follows 6-9 months later. The current pattern shows manufacturing rebounding while services remains steady. This convergence is worth monitoring closely. It could signal a rotation from services-led growth back toward goods-led growth, possibly driven by restocking, reshoring investment, or pre-tariff front-loading. Alternatively, it could be a head-fake where a temporary orders surge masks underlying weakness.

The 2022-2025 cycle was extreme in its bifurcation. Manufacturing contracted for over two years while services barely dipped below 50. If convergence continues and manufacturing moves sustainably above services, that would be genuinely bullish for the goods economy. If manufacturing rolls back below 50, the failed breakout becomes a distribution signal.

ISM Manufacturing Subcomponents: The Story Beneath the Headline

The headline PMI is a composite of five subindices: New Orders, Production, Employment, Supplier Deliveries, and Inventories. Each tells a different story about where in the cycle we are.

Three things stand out:

New Orders at 57.1. This is the most forward-looking subcomponent and it leads the headline PMI by 1-2 months. Orders above 55 historically correlate with manufacturing GDP growth of 3-4%. The strength here is real and suggests the ISM headline has legs, at least for the near term.

Employment at 48.1. This is the red flag. Manufacturing is expanding output without adding workers. That can mean productivity improvements, overtime hours replacing new hires, or management uncertainty about whether the demand surge is permanent. When orders are above 55 but employment is below 50, businesses are telling you they see the demand but don’t trust it enough to commit to headcount. That is a conditional bet, not a full commitment. This is where the Business pillar meets the Labor pillar. If ISM Employment stays below 50 even as orders surge, the labor flows we track won’t deteriorate, but they also won’t improve.

Prices Paid at 59.0. Input cost pressure is returning. This feeds into the inflation picture and complicates the Fed’s path. If manufacturing is re-accelerating with prices rising, the “last mile” of disinflation gets harder, especially in goods prices that had been deflationary for most of 2023-2024.

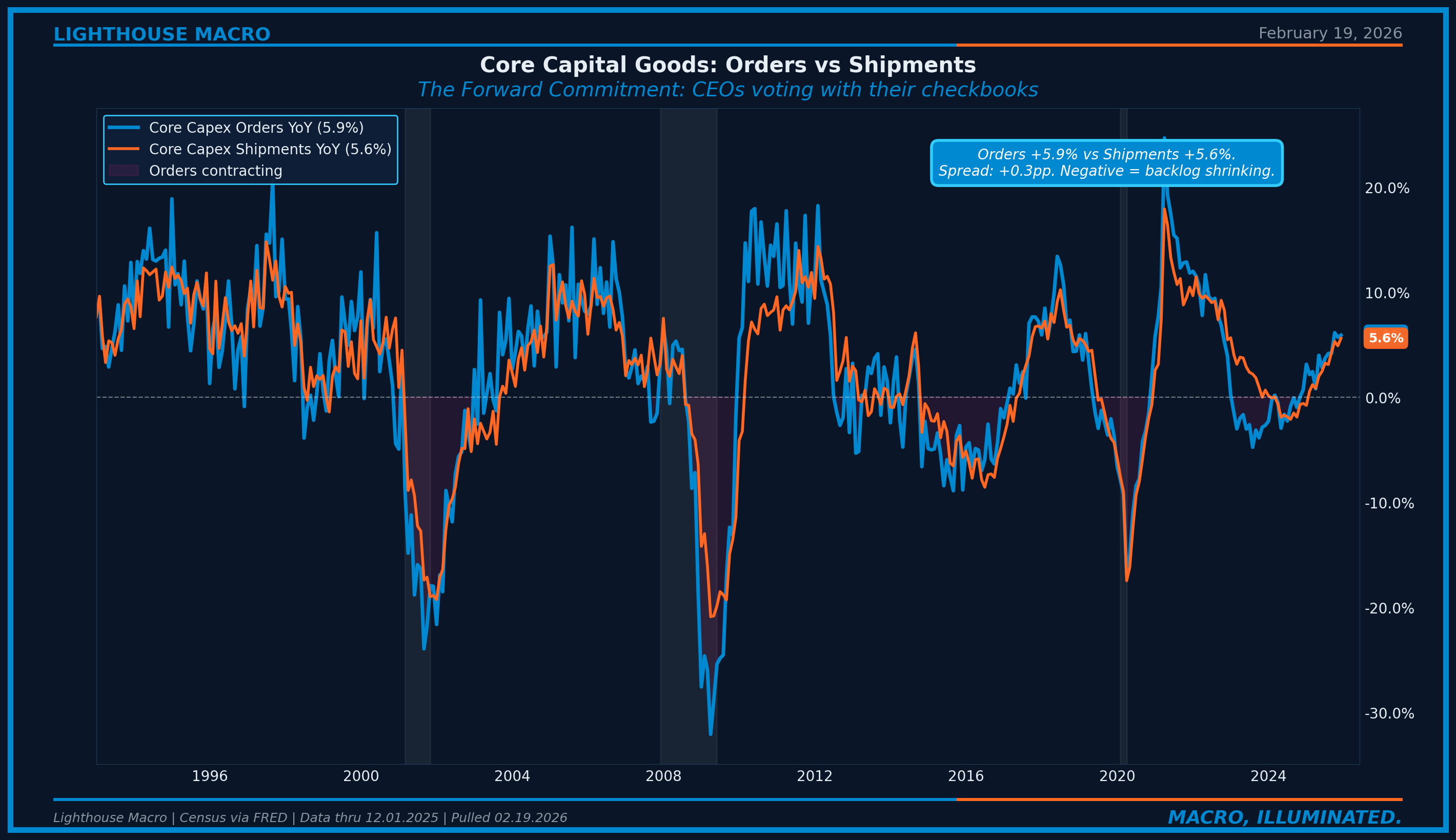

Core Capital Goods Orders: The Forward Commitment

If ISM surveys capture intentions, capital goods orders capture commitments. Core capital goods orders (nondefense, excluding aircraft) strip out the noise from Boeing and defense procurement to reveal what the private sector is actually ordering in terms of equipment, machinery, and technology.

Core capex orders are running at +5.9% year-over-year. That is solidly positive and consistent with a modest expansion, but not the kind of surge that signals a major capex upcycle. Shipments, which measure what’s actually being delivered, are at +5.6%. The narrow spread between orders and shipments means backlogs are roughly stable.

The question is whether this pace of growth reflects genuine investment in new capacity, reshoring supply chains, and technological upgrade cycles, or whether some of it is front-loading ahead of anticipated tariff increases. The 2017-2018 analog is instructive: capital goods orders surged on the back of the Tax Cuts and Jobs Act and anticipated tariffs, then collapsed through 2019 as the front-loading effect wore off. At +5.9%, the current pace is healthy but not extreme enough to suggest aggressive pull-forward. If it accelerates sharply in coming months, the front-loading hypothesis gains weight.

The Bookings/Billings Ratio and Durable Goods

The ratio of orders to shipments (bookings to billings) reveals whether the backlog is growing or shrinking. Above 1.0 means demand exceeds supply. Below 0.95x signals demand failing to keep pace with supply.

. At ~1.00")

At ~1.00x, the bookings-to-billings ratio shows orders roughly matching shipments. Backlogs are stable, not building. That’s consistent with steady-state production rather than an acceleration. It’s not a warning sign, but it’s not a growth signal either. Factories are filling orders at roughly the rate they’re receiving them.

Total durables at +10.0% YoY versus ex-transportation at +5.1% tells you Boeing orders are inflating the headline. At +5.1%, ex-transport is solidly positive but not as euphoric as the total suggests. The direction is right, the magnitude is modest.

Business Inventories: The Mistake Detector

Inventories are where optimistic forecasts go to die. When businesses build inventory expecting demand that doesn’t arrive, the result is a liquidation cycle: production cuts, order cancellations, and layoffs to burn through the excess. The inventory-to-sales ratio is the diagnostic tool.

The I/S ratio at 1.37 is in the balanced zone. Below 1.35 means inventories are lean (bullish for production). Above 1.40 means inventories are elevated relative to sales (bearish, liquidation risk). At 1.37, there is no immediate overhang. Inventory growth has moderated to +1.2% year-over-year, down from double-digit growth during the 2021-2022 post-COVID restocking surge.

This is quietly good news. One of the key risks in any manufacturing recovery is an inventory overshoot where orders surge, production ramps, but final demand doesn’t follow. The lean I/S ratio suggests businesses learned from the 2021-2022 bullwhip effect and are managing stock more carefully this cycle.

Regional Fed Manufacturing Surveys: The ISM Preview

Five regional Federal Reserve banks publish their own manufacturing surveys before the national ISM release. Taken together, they provide a 2-3 week preview of where ISM is heading.

The five-survey average sits at 2.2, barely in expansion territory and well below where the ISM’s 52.6 would imply. That divergence matters. Either the regionals catch up in coming months (confirming the ISM breakout) or the ISM reverts downward (the breakout was noise). The resolution will take 2-3 months. District-level dispersion reinforces the skepticism: Philly is the strongest at +12, while Richmond sits at -6 and Kansas City at -2. The manufacturing recovery, if it is one, is geographically uneven.

Industrial Production & Capacity Utilization: Output Meets Constraint

Industrial production measures actual factory output. Capacity utilization measures what percentage of available production capacity is being used.

IP growth at +2.3% year-over-year is positive but modest. The more important number is capacity utilization at 75.5%. The 78% threshold matters because above it, factories start competing for labor, equipment, and materials, which generates pricing power and inflation. Below it, there is slack in the system. At 75.5%, manufacturing has room to expand output without triggering inflationary bottlenecks.

This is the tension in the current picture. ISM says manufacturing is expanding robustly. Capacity utilization says there’s plenty of room to absorb that expansion without overheating. That’s actually a goldilocks scenario for the near term, if it lasts.

Corporate Profits: The Bottom Line

Revenue is vanity. Profits are sanity. Corporate profits before tax capture what actually flows to the bottom line after businesses pay their workers, suppliers, and overhead. Profits peak before the economy does and trough before the economy does. They are both a coincident indicator of business health and a leading indicator of future hiring and investment decisions.

YoY, 2000-2026. Profits growing at +4.")

Corporate profits before tax are growing at +4.3% year-over-year (Q3 2025, BEA). Positive, but hardly booming. This is the kind of modest profit growth that sustains the status quo without triggering a new hiring or investment wave. It keeps businesses from cutting costs aggressively, but it doesn’t give them a reason to expand headcount either. That is consistent with ISM Employment below 50: the order book is full enough to avoid layoffs, thin enough to avoid hiring.

The historical pattern matters here: profits peak before the economy does and trough before the economy does. At +4.3%, profits are decelerating from the double-digit growth rates of 2021-2022, and the direction of travel matters more than the level. When profit growth decelerates toward zero, businesses shift from expansion mode to preservation mode. The first cuts are discretionary spending (travel, consulting, marketing). Then headcount. We’re not there yet, but the trajectory is worth watching closely. If profits decelerate further through Q1 2026, the labor market should start reflecting that caution by late 2026.

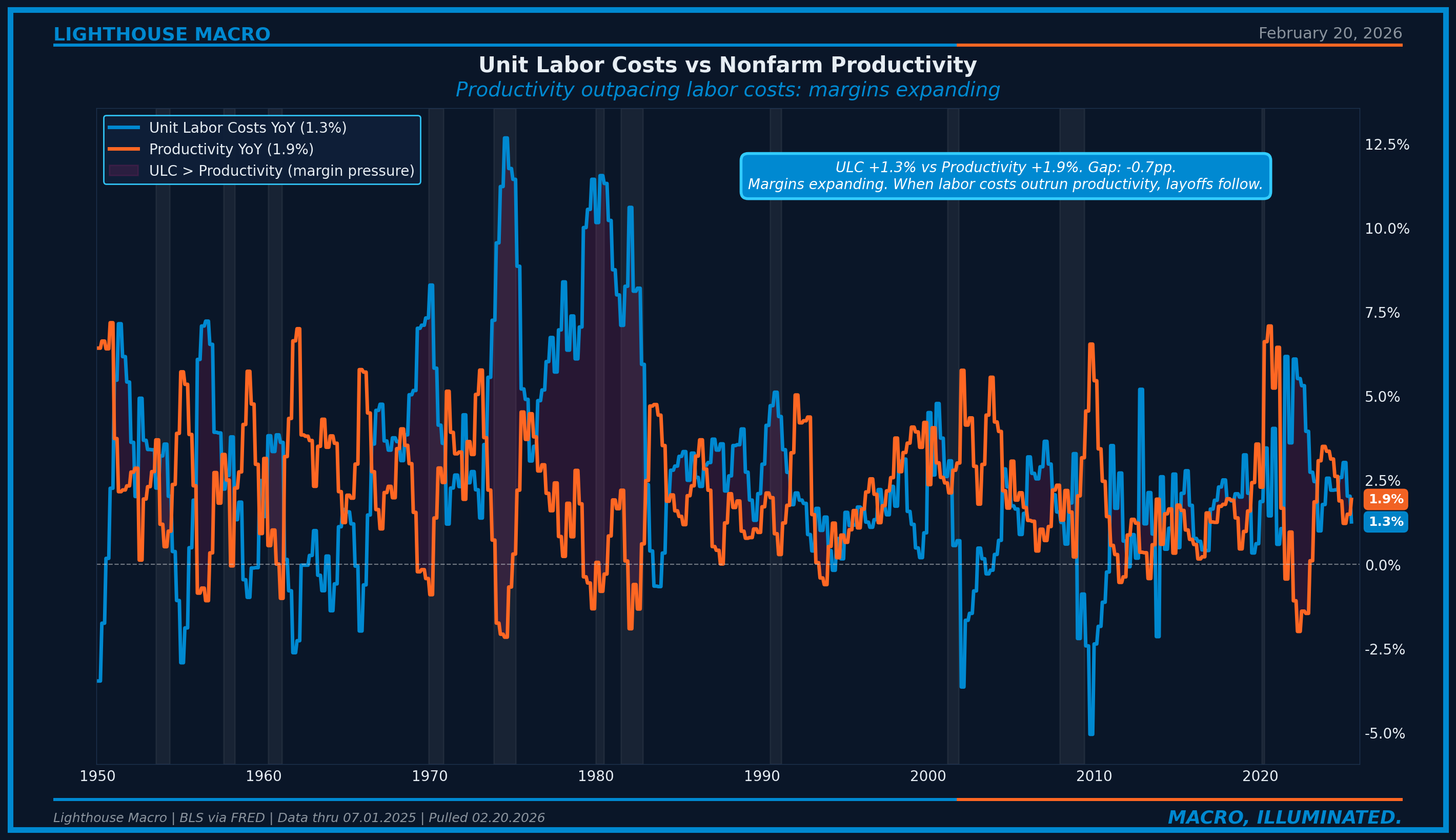

Unit Labor Costs vs Productivity: The Margin Squeeze

The relationship between unit labor costs and productivity determines margin direction. When productivity growth exceeds labor cost growth, margins expand. When labor costs outrun productivity, margins compress. Simple arithmetic, profound consequences.

The good news: unit labor costs at +1.3% are running below productivity growth at +1.9%. The -0.7 percentage point gap means margins are expanding at the aggregate level. This is consistent with the modest profit growth we see in the BEA data (+4.3%) and helps explain why businesses aren’t cutting costs aggressively. As long as productivity continues to outpace labor costs, the profit picture remains stable. The risk is if tariff-driven input cost pressure (ISM Prices Paid at 59.0) starts eating into margins faster than productivity gains can offset. That would turn modest profit growth into stagnation, and stagnation into cuts.

Business Loans & Delinquency: The Credit Channel

Credit is the lubricant of business expansion. When loan growth is positive and delinquencies are low, businesses have access to capital and the confidence to use it.

C&I loan growth at +3.0% year-over-year is positive but unremarkable. Compared to the +12-15% growth rates seen during expansion peaks, current lending is restrained. Business loan delinquencies at 1.3% are elevated versus the 0.8-0.9% lows of 2022 but well below the 4%+ levels that signal systemic stress.

The credit channel is not constraining business expansion, but it is not amplifying it either. Banks are lending cautiously. Borrowers are borrowing selectively. Mid-cycle normalization, not a credit crunch.

Conference Board Leading Economic Index: The Composite Crystal Ball

The LEI aggregates 10 forward-looking economic indicators into a single composite: manufacturing new orders, building permits, stock prices, credit spreads, consumer expectations, and the yield curve. (Note: the Conference Board restructured the LEI’s components in 2023, which affects direct comparisons with pre-2023 readings.) When the LEI declines year-over-year by more than 4% for six or more months, a recession has historically followed.

The LEI fell 0.2% in December 2025 to 97.6, extending its decline. Year-over-year, it remains near -3.7% and has been negative for over two years. This is one of the longest sustained declines on record without a recession materializing. Two interpretations compete. The bull case: the LEI is structurally impaired by the inverted yield curve component, which has been sending a false signal in an era of term premium distortion. Remove the yield curve component, and the LEI looks less alarming. The bear case: the LEI’s signal is being delayed, not negated, because fiscal spending and excess savings provided unusual buffers that merely extended the lag between signal and recession. Those buffers are now largely exhausted.

Either way, the LEI has not confirmed the manufacturing breakout. Until it does, the ISM surge exists in tension with the broader leading indicator framework.

The Consensus Trap

The consensus narrative on the business cycle right now falls into one of two camps, and both are oversimplified.

Camp 1: “Manufacturing is back.” ISM above 50, capex orders positive, new orders strong. Buy industrials, buy materials, buy the cyclical rotation.

Camp 2: “The LEI is still negative.” Leading indicators declining for over two years, capacity utilization showing slack, employment not following. The ISM breakout is noise. Stay defensive.

Both camps are cherry-picking. Camp 1 ignores that ISM at 52.6 is barely in expansion, employment hasn’t followed, and regional surveys at 2.2 aren’t confirming. Camp 2 ignores that new orders at 57.1 are genuinely strong, capex growth is positive, and profits (while modest) aren’t contracting. The sharper question: does the new orders strength translate into sustained expansion with employment and profits accelerating, or is this a front-loaded burst that fades once pre-tariff orders are filled? The employment subcomponent is the tell. If ISM Employment stays below 50 even as orders surge, businesses are hedging. They see the demand but don’t trust it. That conditional posture resolves one way or another within 2-3 quarters.

Where We Are Now

Current readings across the business framework:

Net assessment: Survey data says expansion. Hard data on orders confirms. Profits are positive but not accelerating. The LEI remains in warning territory and capacity utilization shows ample slack. This is a conditional expansion: strong as long as orders keep flowing, vulnerable the moment demand normalizes. The employment subcomponent at 48.1 tells you businesses themselves are hedging, filling orders with existing capacity, not building for the future.

How to Track This

Monthly cadence:

1. First business day: ISM Manufacturing PMI. The headline and the subcomponents. Watch New Orders (lead indicator) and Employment (commitment indicator).

2. Third business day: ISM Services PMI. Watch for convergence or divergence with manufacturing.

3. Regional Feds (mid-month): Empire State (NY Fed), Philly Fed, Richmond Fed, Dallas Fed, Kansas City Fed. Individually noisy, collectively useful as ISM preview.

4. Last week of month: Durable Goods Orders (Census). Core capital goods orders and shipments. The bookings/billings ratio.

5. Quarterly: Corporate Profits (BEA, lagged 2 months). Unit Labor Costs and Productivity (BLS). LEI (Conference Board, monthly but most informative on a quarterly trend basis).

Key relationships:

• New Orders lead the headline PMI by 1-2 months

• ISM leads Industrial Production by 2-3 months

• Capital goods orders lead actual investment spending by 3-6 months

• Profits lead hiring/firing decisions by 2-4 quarters

• Regional Fed surveys lead ISM by 2-3 weeks

Invalidation Criteria

Bull Case (Sustained Manufacturing Recovery) Confirmation:

• ISM Manufacturing holds above 52 for 3+ consecutive months

• ISM Employment returns above 50 (businesses hiring, not just filling orders)

• Regional Fed 5-survey average rises above 10

• Corporate profits accelerate above +8% YoY growth

• LEI turns positive year-over-year

• Capacity utilization crosses above 78%

Current status: One of six conditions met (ISM above 52, one month of data).

Action if confirmed: Increase cyclical exposure. Overweight industrials, materials, and mid-cap equities with manufacturing leverage. Core capex orders at current levels support a 6-12 month positive outlook for the goods economy.

Bear Case (Profit-Led Downturn) Confirmation:

• Corporate profits contract for 3+ consecutive quarters

• ISM Manufacturing rolls back below 48

• Core capex orders turn negative year-over-year

• I/S ratio exceeds 1.45 (inventory overshoot)

• Business loan delinquencies rise above 2.0%

• ISM Employment drops below 45

Current status: Zero of six conditions met.

Action if confirmed: Reduce cyclical exposure. Underweight small caps and industrials. Monitor credit spreads for stress acceleration. The profit-to-layoff transmission typically takes 2-4 quarters.

The Bottom Line

Business investment is the economy’s forward commitment. Surveys tell you what businesses intend to do. Orders tell you what they’ve committed to. Inventories tell you when they got it wrong. Profits tell you whether it’s working.

Current conditions: conflicted. The ISM breakout above 50 after manufacturing spent the better part of three years in contraction is a meaningful signal. Core capex orders at +5.9% confirm businesses are investing. Profits at +4.3% are positive, not crashing. But employment isn’t following, regional surveys are barely above zero, capacity utilization shows ample slack, and the LEI remains in warning territory. The expansion is real but conditional.

Watch the employment subcomponent. When businesses start hiring into the order surge, that’s confirmation the expansion is sustainable. As long as they’re filling orders with existing capacity and overtime, they’re telling you they don’t trust it yet. Neither should you.

This is how we analyze the business cycle.

This is the 6th in a 12-part series on the Lighthouse Macro framework.

Next up: Trade & the Dollar.

Bob Sheehan, CFA, CMT

Founder & Chief Investment Officer, Lighthouse Macro