Consumer: The Last Domino

The Diagnostic Dozen: A Framework for Reading the Macro Cycle (4 of 12)

Previously in this series: Labor | Prices | Growth

The consumer is not a leading indicator. It is a lagging confirmation of what labor, credit, and confidence already told you. And it represents 68% of GDP.

That is the paradox. Personal Consumption Expenditures is the single largest component of economic output. When consumer spending contracts, there is nowhere for GDP to hide. Yet by the time that contraction arrives, labor already cracked 6-9 months prior, credit stress was visible in delinquency data, and confidence surveys had been deteriorating for two quarters. The consumer is the last domino.

This is why most consumer analysis gets the sequencing wrong. Headlines celebrate “resilient consumer spending” while the fuel tank that supports that spending is draining. The question is not just “is the consumer spending?” It is “what is funding the spending, and how long can it last?”

The Core Insight: Income vs Credit

Here is the conceptual unlock that separates useful consumer analysis from headline-watching.

Consumer spending has only two funding sources: income and credit. When spending is funded by income growth (wages rising, employment expanding, hours stable), the spending is sustainable. When spending is funded by credit (savings depleted, credit card balances rising, delinquencies climbing), the spending is borrowed from the future.

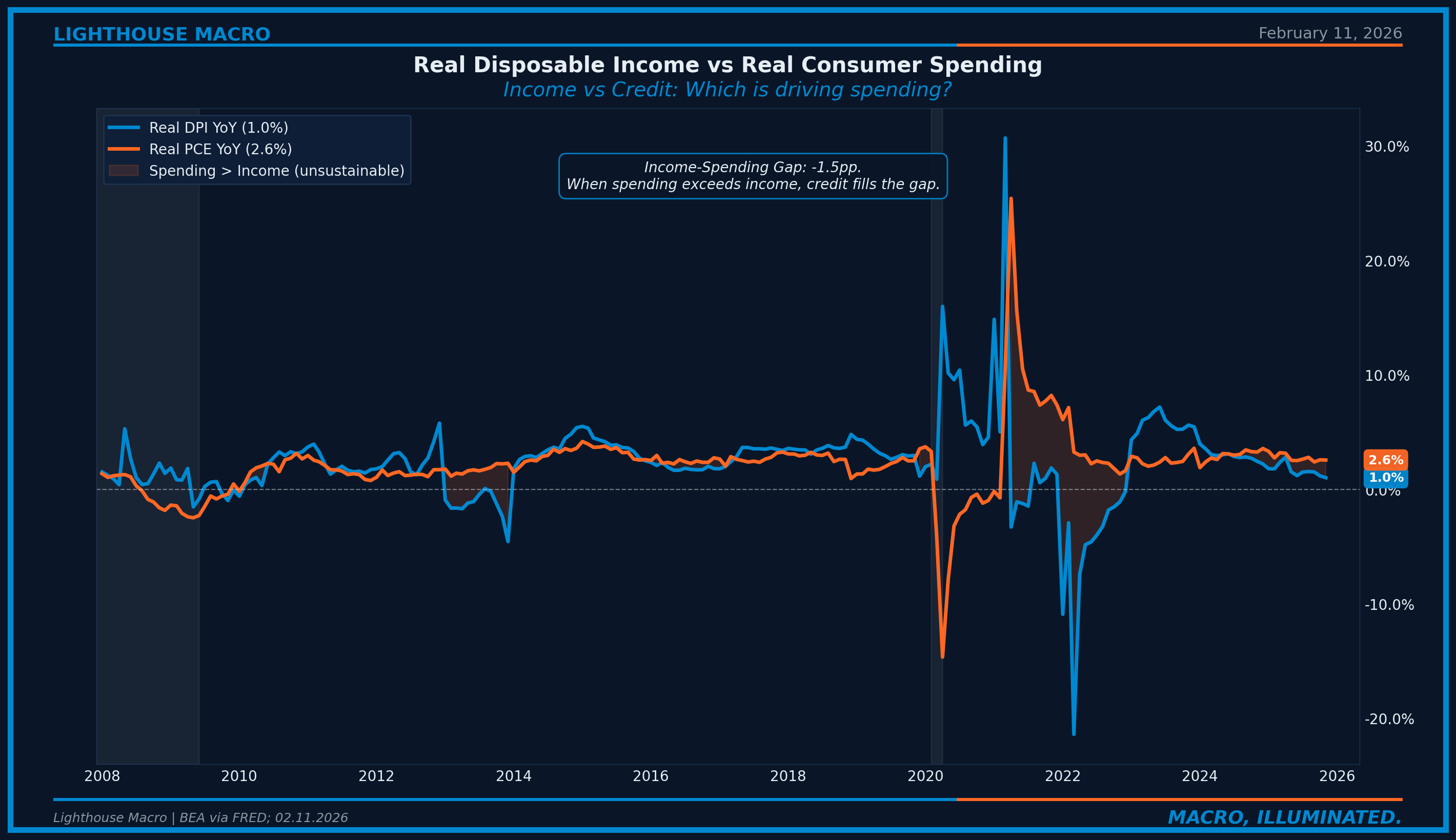

The distinction matters because the two regimes look identical in the headline data. Real PCE at +2.6% tells you nothing about whether that spending is income-driven or credit-driven. Both produce the same GDP print. But one is sustainable and the other is a countdown timer.

We track this through what we call the Three-Stage Stress Sequence. It operates the same way every cycle:

Stage 1: Savings Depletion. Income growth slows but spending habits persist. Consumers draw down savings to maintain lifestyle. The saving rate falls. This can persist for 12-18 months.

Stage 2: Credit Substitution. Savings exhausted, consumers turn to credit. Credit card balances rise. Delinquencies begin climbing. Interest payments consume a growing share of income. This stage is inherently unstable.

Stage 3: Spending Collapse. Credit dries up or becomes unaffordable. Spending contracts. Durables first (big-ticket deferrals), then nondurables, then eventually services. Corporate revenues fall. Layoffs begin. The reinforcing loop turns vicious.

The chart makes the dynamic visible. When the orange line (spending) runs above the blue line (income), consumers are spending more than they earn. Something else is funding the difference. In 2020-2021, it was stimulus checks and savings accumulation. Today, it is credit. The income-spending gap currently stands at -1.5 percentage points. Spending growth of +2.6% is outrunning income growth of +1.0%. That arithmetic has an expiration date.

What to Watch and Why

We approach consumer analysis through three lenses. Not a checklist, but a framework for organizing the signal from the noise.

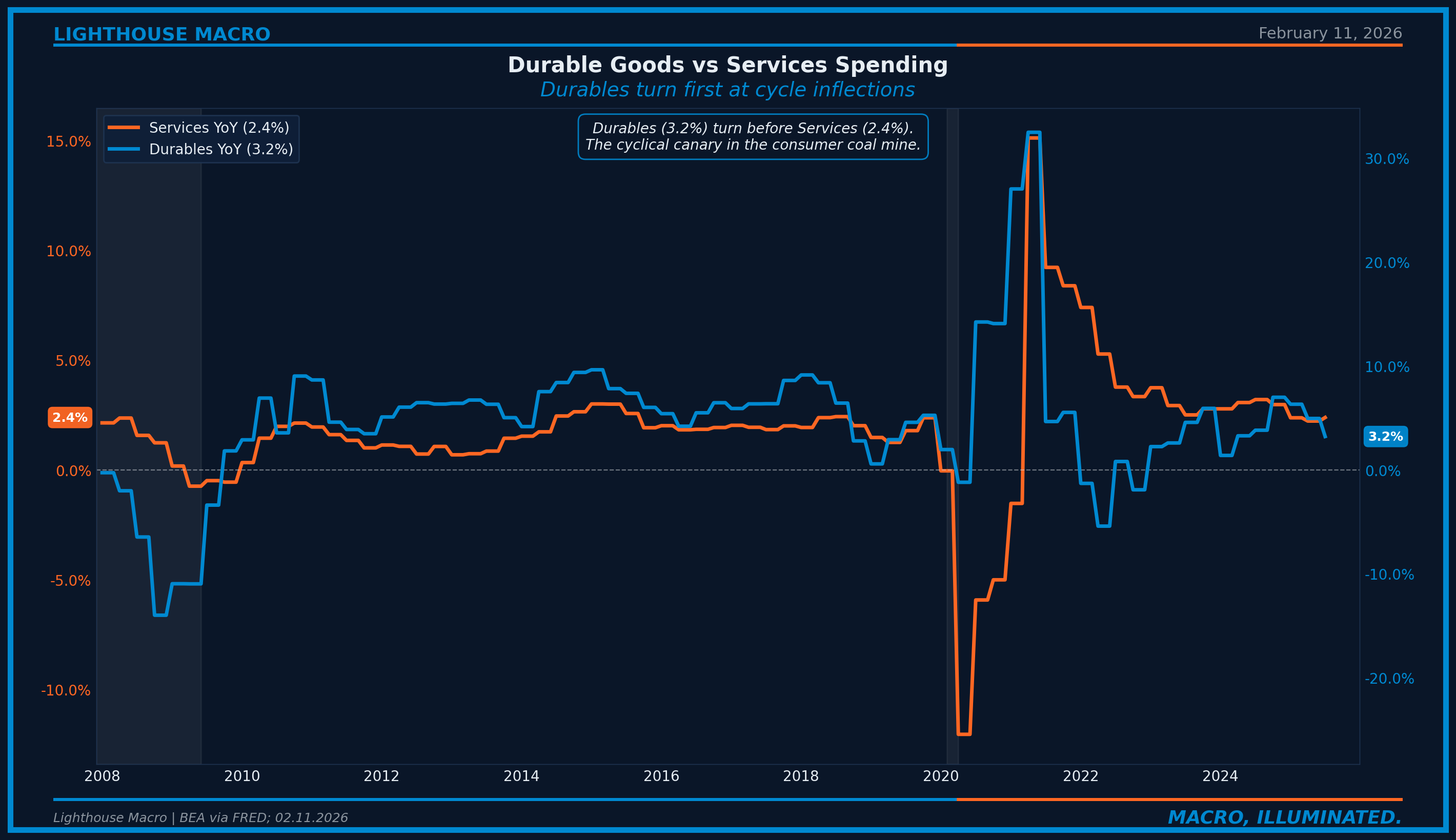

Spending flows capture what consumers actually do. Personal Consumption Expenditures, retail sales, credit card transactions. These are output variables: the result of income, confidence, and credit availability interacting. Spending flows tell you where the economy is, not where it is going. Watch the composition (durables vs services) more than the aggregate. Durables turn first at cycle inflections because consumers defer big-ticket purchases before cutting everyday spending.

The fuel tank captures what is funding the spending. Income growth (aggregate payrolls: employment times hours times wages), the saving rate, and disposable income. When the fuel tank is full (saving rate above 7%, real income growing 2%+), spending can persist. When it is empty (saving rate below 4%, real income barely positive), spending is running on fumes.

Stress signals capture the cracks forming beneath the surface. Credit card delinquencies, the debt service ratio, consumer confidence indices. These are the early warning system. Delinquencies lead spending cuts by 3-6 months. Confidence surveys lead spending by 1-3 months. The stress signals flash before the spending data confirms.

The discipline is triangulating across all three. When spending flows are positive but the fuel tank is draining and stress signals are rising, you are watching Stage 2 of the stress sequence. The headline looks fine. The foundation is eroding.

The Indicators That Matter

Personal Consumption Expenditures: The 68% Anchor

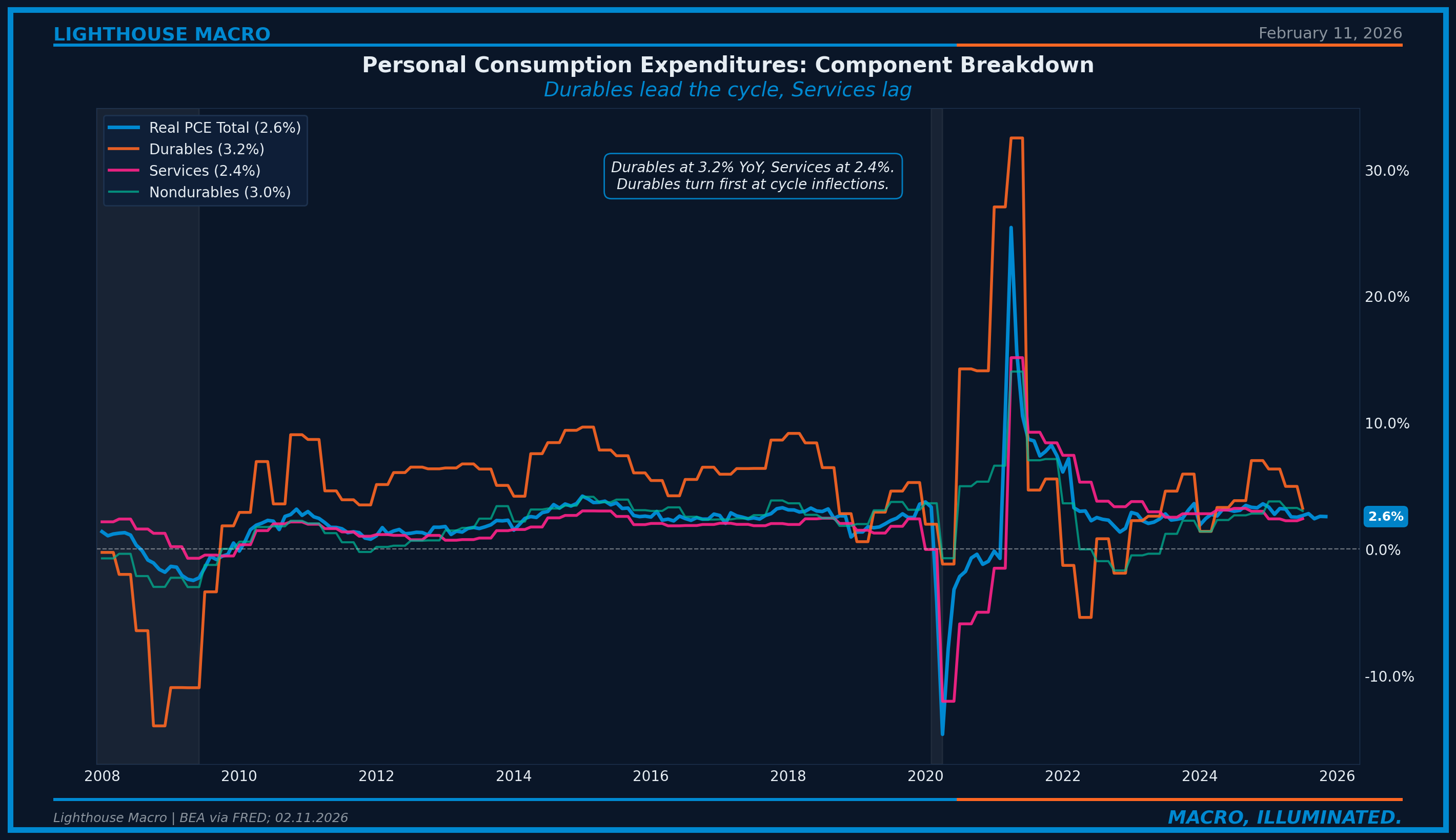

PCE is the largest GDP component. It breaks into three pieces: durable goods (cars, appliances, furniture), nondurable goods (food, gasoline, clothing), and services (healthcare, housing, dining, travel). Services alone represent nearly 70% of total PCE.

Why the decomposition matters: durables are the cyclical canary. When consumers lose confidence, they defer big-ticket purchases first. You do not need a new car this quarter. You do need groceries. Durable goods spending peaked at +32% YoY in April 2021 (the post-COVID stimulus surge) and has been normalizing since. Nondurables are stable. Services are sticky (lease contracts, subscriptions, healthcare obligations create inertia).

The chart shows the pattern. Durables swing wildly (the COVID spike and normalization dominate the picture). Services are steadier. At cycle turns, watch for durables to decelerate or contract while services hold. That divergence is the early signal that the consumer is pulling back on discretionary spending while maintaining essentials.

Current reading: Real PCE is growing at +2.6% year-over-year. The headline looks solid. But December 2025 retail sales came in flat (0.0% month-over-month, below +0.4% consensus), with the control group at -0.1%. The monthly data is catching up with what the flow dynamics already suggest. This is the aggregate number, and the aggregate can deceive. We need to look beneath it.

The Saving Rate: The Fuel Gauge

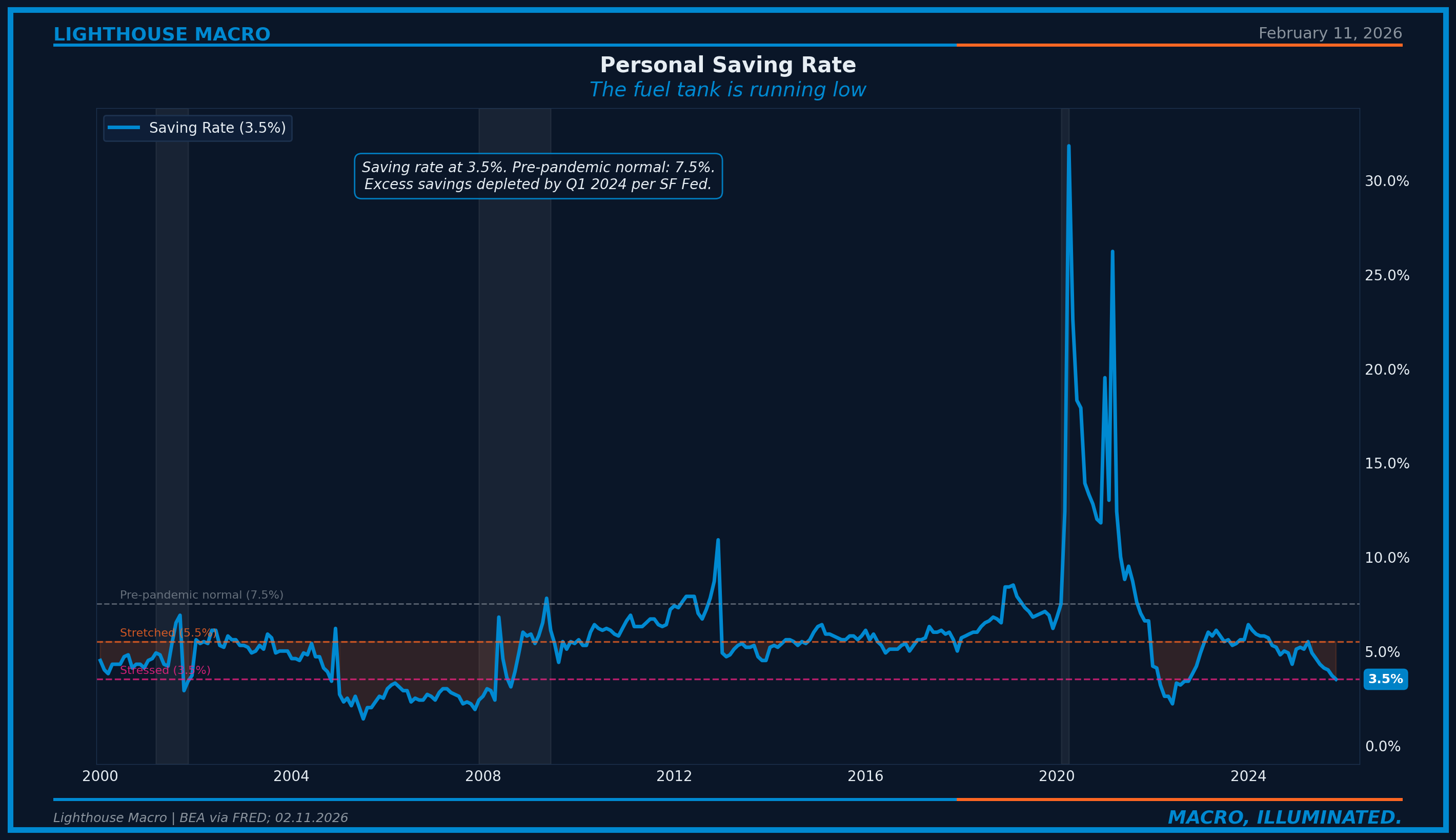

The personal saving rate measures what percentage of disposable income is not spent. It is the buffer. When the saving rate is high, consumers have capacity to absorb shocks (job loss, unexpected expenses, rate hikes). When it is low, there is no cushion. Every dollar earned is already spoken for.

Why it works as a leading indicator: the saving rate signals future spending capacity. A falling saving rate means consumers are spending an increasing share of income. That can persist for a while, but it reduces the margin for error. When it drops below 4%, consumers are effectively living paycheck-to-paycheck in aggregate.

The saving rate peaked at ~33.8% in April 2020 (stimulus checks with nowhere to spend them, revised upward in the BEA’s 2023 NIPA update). The excess savings accumulated during COVID (~$2.1 trillion per the SF Fed) were fully depleted by Q1 2024. The SF Fed’s savings tracker was subsequently discontinued after September 2024. At 3.5%, consumers are at the “stressed” threshold. The buffer has been gone for nearly two years. Stage 1 is not just complete, it is ancient history. The next question: what replaces savings?

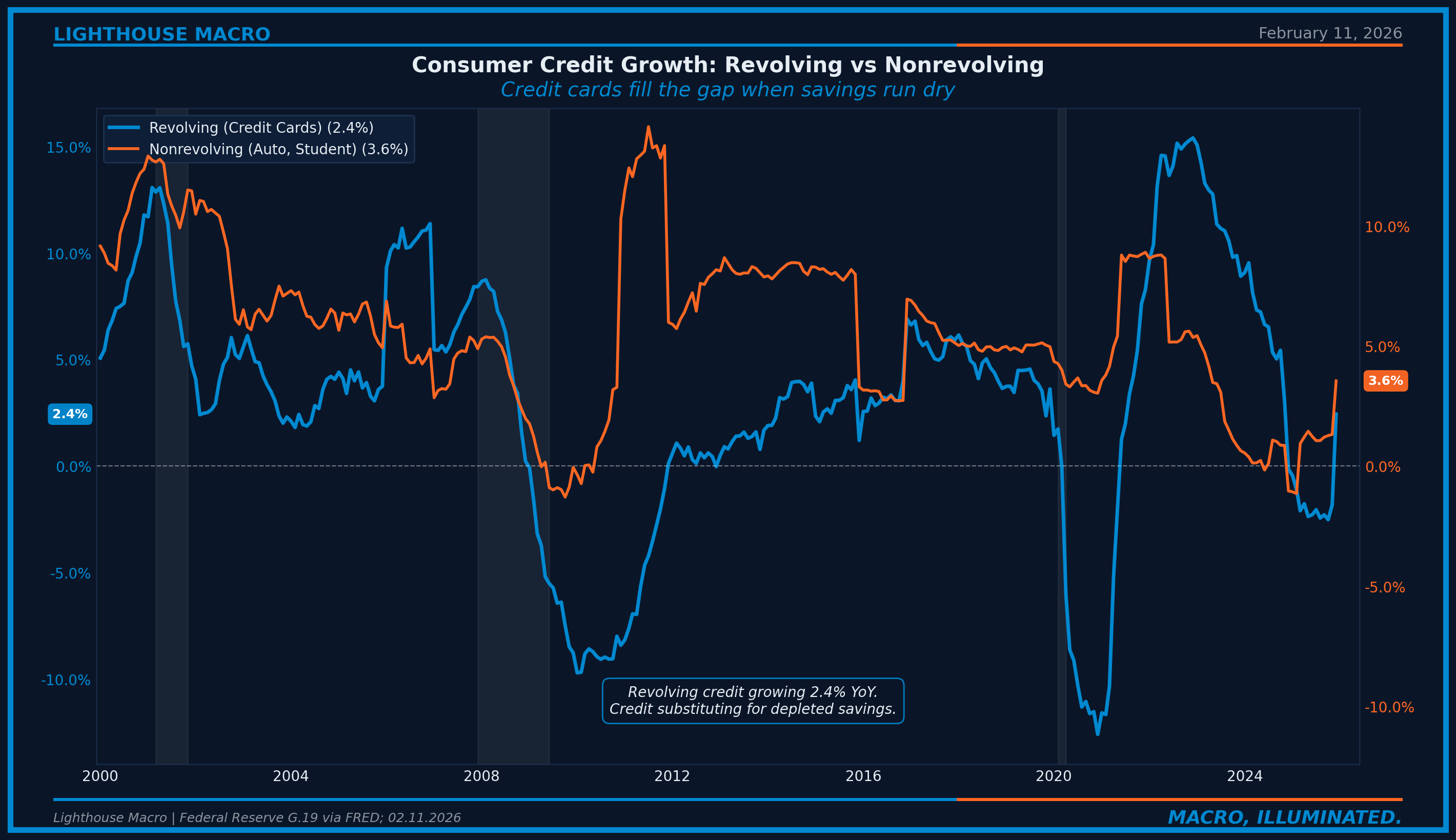

Consumer Credit: The Accelerant and the Warning

When savings run out, consumers turn to credit. Rising credit balances are not inherently problematic. Credit greases the wheels of commerce. The problem emerges when credit substitutes for income rather than supplementing it. When balances rise while delinquencies climb, that is not healthy credit expansion. That is desperation.

Revolving credit (credit cards) is the stress indicator. Per the Fed’s G.19 release (January 8, 2026), credit card debt specifically grew +3.4% YoY in 2025, outpacing the total consumer credit growth rate of +2.4%. Nonrevolving credit (auto, student) grew a more subdued 2.0%. Credit card debt carries APRs averaging 22.3% for cardholders carrying balances, making it the most expensive form of consumer borrowing. Both rates have been declining since the Fed began cutting in September 2024, but the starting point was so elevated that relief is marginal. When consumers lean on credit cards to fund everyday spending, the interest burden compounds quickly. Nonrevolving credit (auto loans, student loans) is more structural and less cyclical.

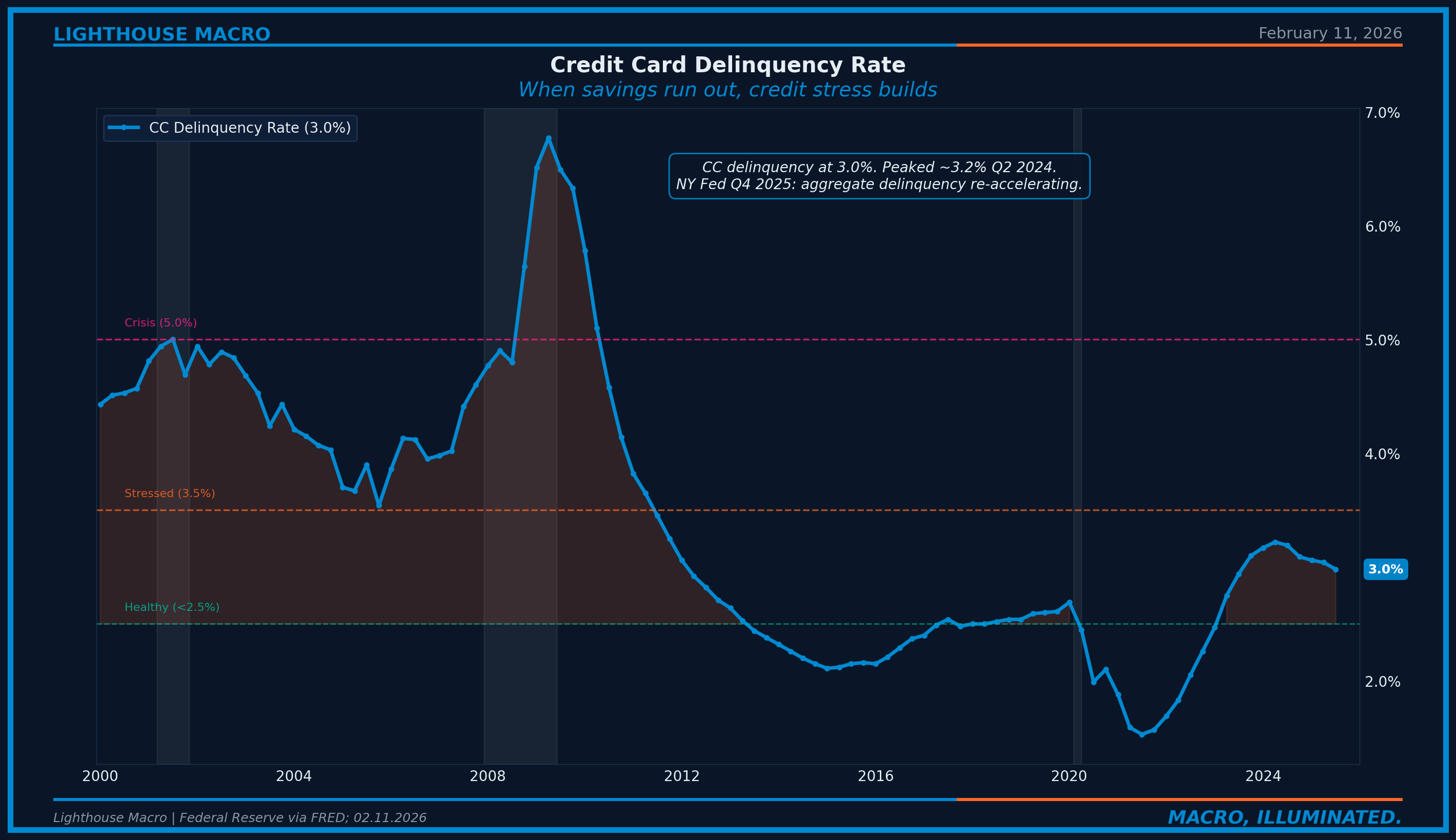

The delinquency trajectory tells the story. Credit card delinquencies bottomed at 1.5% in 2021 when stimulus checks and forbearance programs suppressed defaults. They doubled to ~3.2% by Q2 2024, the highest level since 2012. Through Q3 2025, the credit card rate had been declining for five consecutive quarters to 3.0%, suggesting stabilization. Then the NY Fed’s Q4 2025 Household Debt Report (released February 10, 2026) showed a broader re-acceleration: aggregate delinquency across all debt types worsened to 4.8% from 4.5%, with credit card transitions into serious delinquency ticking back up. These are different metrics: the 3.0% is credit card-specific (Fed), the 4.8% is all household debt combined (NY Fed). Both are moving in the wrong direction. This is not crisis territory (the GFC peak for credit cards was 6.8%), but the trend reversal is significant. Delinquencies lead charge-offs by 3-6 months. Charge-offs lead bank lending tightening by another quarter. The transmission chain is in motion.

The 3.5% threshold is where stress transitions from “manageable” to “problematic.” At 5.0%, regional banks with concentrated consumer lending portfolios face capital impairment. Credit stress does not resolve itself. It transmits.

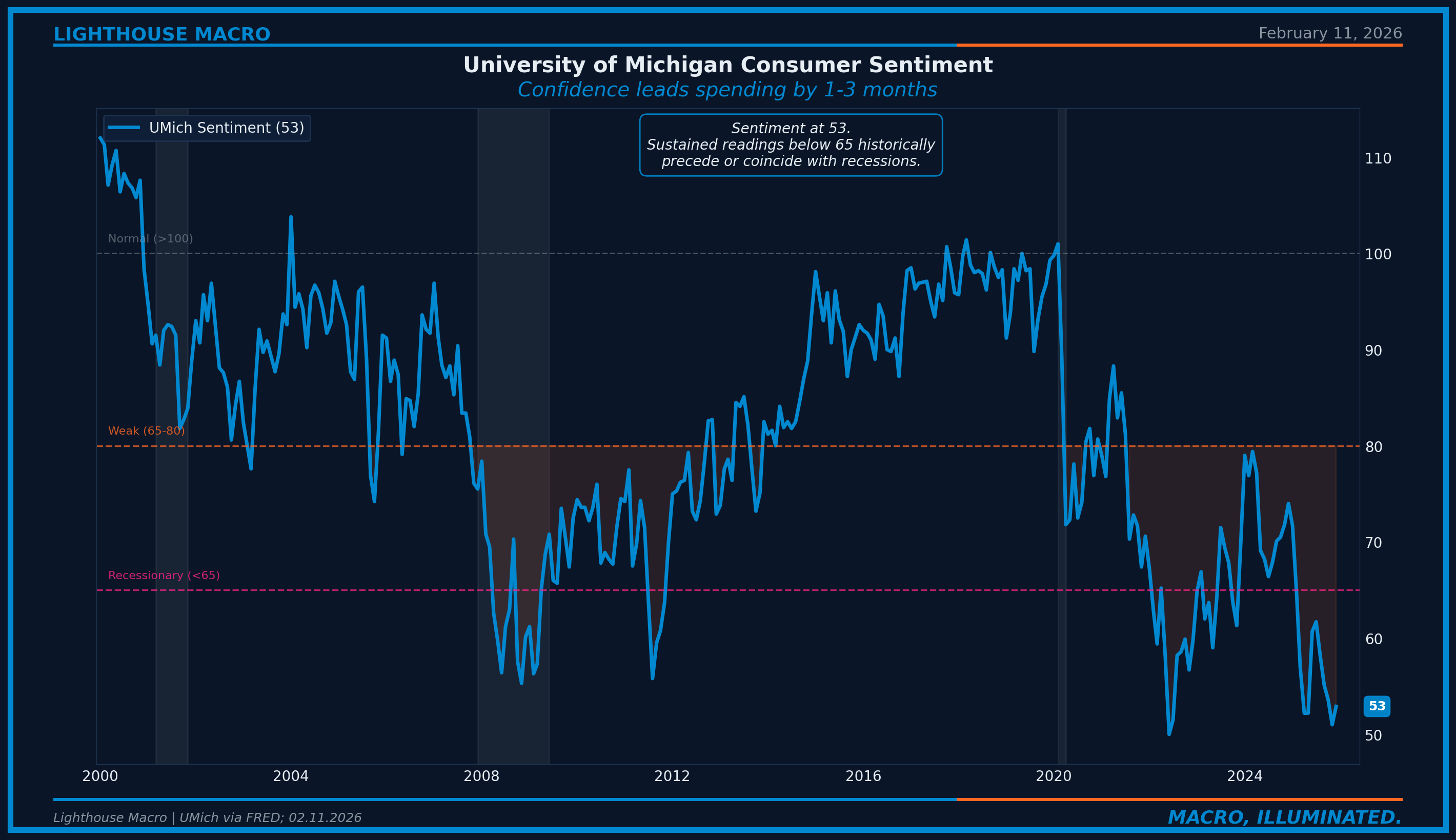

Consumer Confidence: The Psychological Driver

Confidence surveys measure expectations, not outcomes. They tell you what consumers plan to do, not what they have done. That makes them noisy but potentially leading.

We track two primary surveys. The University of Michigan Consumer Sentiment Index, measured consistently since the 1960s, captures the broader consumer mood. The Conference Board Consumer Confidence Index focuses more on labor market perceptions and forward expectations, making it a sharper cyclical signal.

UMich sentiment bottomed at 53 in December 2025 before recovering modestly to 56.4 in January and 57.3 in the February preliminary reading. The bounce is real but modest, still well below the 65 threshold that historically coincides with or precedes recessions. For context, it hit 50 during the June 2022 inflation shock before recovering to the high 70s.

But the more alarming signal is from the Conference Board. Consumer Confidence plunged to 84.5 in January 2026, the lowest reading since May 2014 and below pandemic-era levels. The Expectations Index fell to 65.1, well below the 80 threshold that historically signals recession within the next year. UMich bouncing modestly while Conference Board collapses suggests current conditions are stabilizing but forward expectations are deteriorating. That divergence is not reassuring.

The important caveat: confidence surveys have become increasingly partisan since 2016. The signal is noisier than it used to be. That said, when both major surveys are this weak, even accounting for partisan distortion, something real is happening. When consumers feel this pessimistic, spending decisions follow. The buying conditions sub-index is particularly useful: it asks whether now is a good time to buy large household items. When buying conditions deteriorate, durable goods purchases follow with a 1-3 month lag.

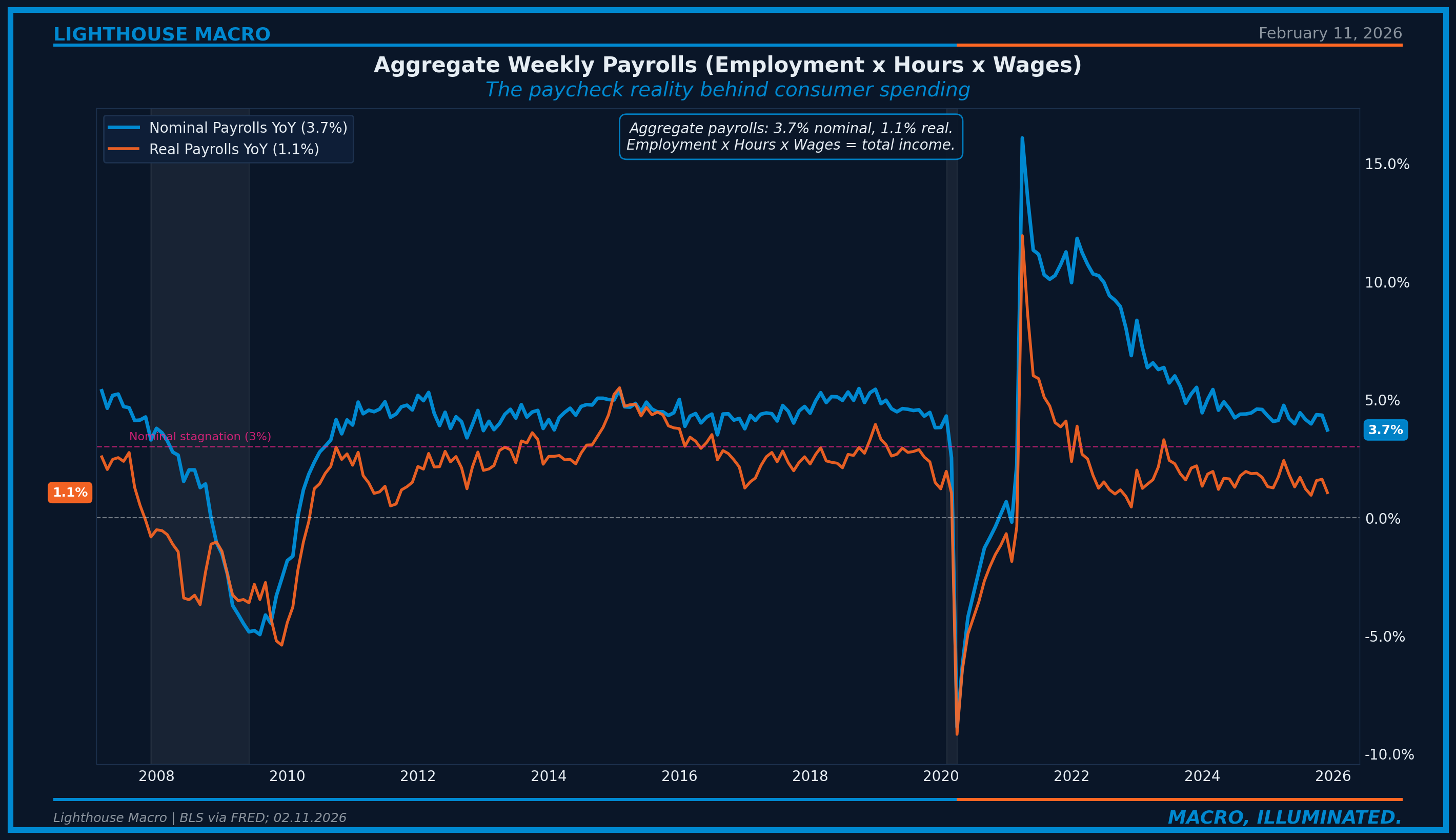

Aggregate Payrolls: The Paycheck Reality

Consumer spending is ultimately funded by paychecks. Aggregate weekly payrolls (employment times average weekly hours times average hourly earnings) capture the total income flowing into the economy each week. This is the fundamental driver. Everything else, savings, credit, confidence, operates in relation to this baseline.

Current configuration: Aggregate payrolls are growing +3.7% nominal, +1.1% real. Those numbers sound adequate, but they represent a deceleration. At the start of 2024, nominal payroll growth was running above 5%. The slowdown reflects all three components fading: employment growth decelerating, average weekly hours declining to 34.1, and wage growth moderating. The tailwind that supported consumer spending through 2023-2024 is losing force.

The January 2026 employment report (released February 11) adds important context. Headline payrolls added 130,000 jobs, above consensus. But cumulative benchmark revisions subtracted 898,000 jobs from 2025 totals. The average monthly gain for 2025 was just 15,000 after revisions, far weaker than previously reported. Federal government employment fell 34,000 (DOGE-related separations beginning to show up). The income pillar is weaker than previously understood. The Employment Cost Index reinforces this: ECI rose only 0.7% in Q4 2025, the slowest quarterly pace since 2021, indicating wage growth is decelerating beneath headline average hourly earnings figures.

The connection to our labor pillar is direct. We covered in Post 1 how the quits rate leads income growth by 6-9 months. When workers stop quitting, wage growth slows. When wage growth slows, aggregate payroll growth slows. When payroll growth slows, the fuel tank drains faster. The transmission chain is mechanical.

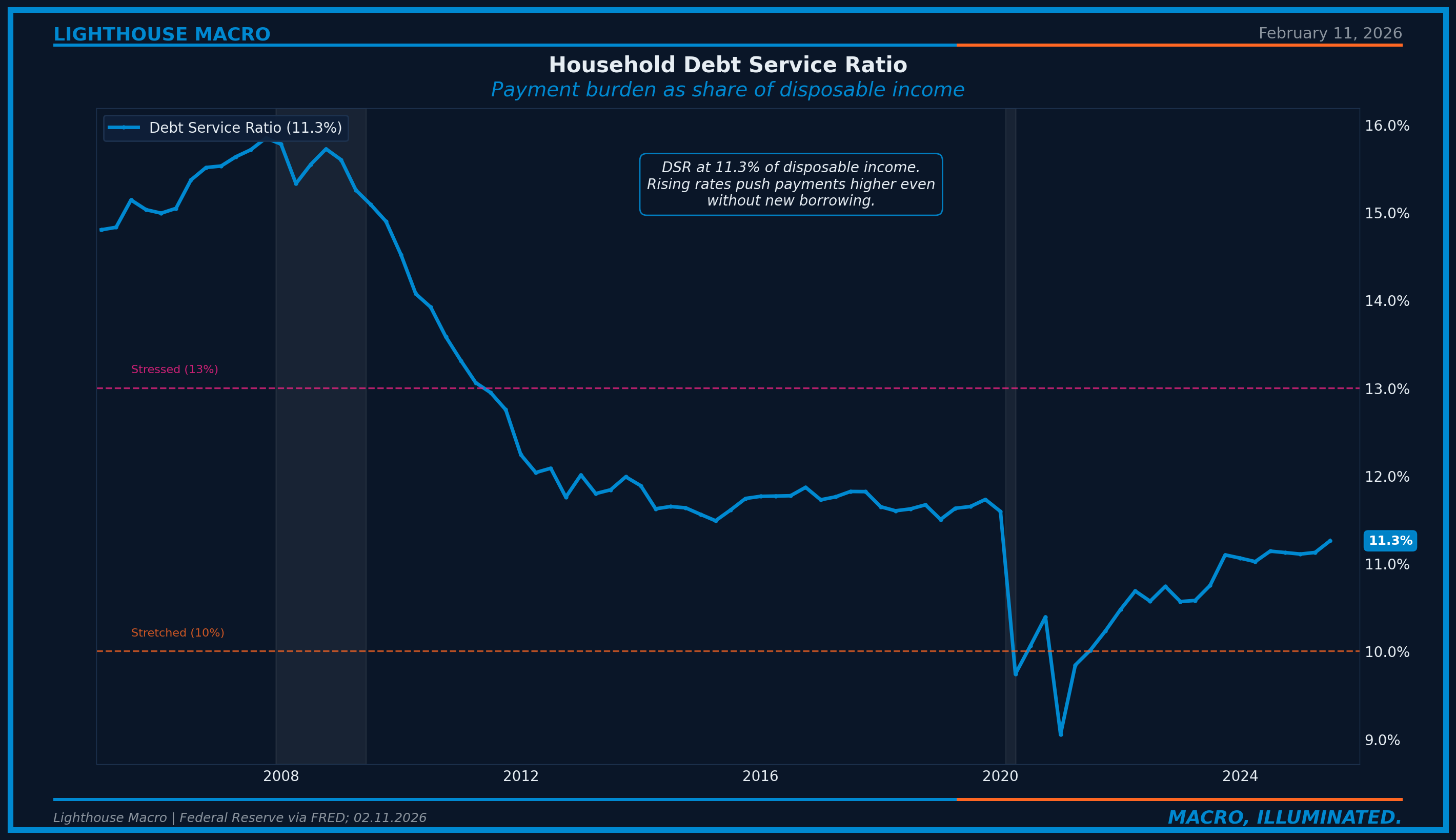

The Debt Service Ratio: The Payment Burden

The household debt service ratio measures required debt payments (mortgage, auto, credit card, student loan) as a percentage of disposable income. It captures how much of each paycheck is already committed to servicing existing debt. The higher the ratio, the less discretionary spending power remains.

The DSR bottomed at 9.1% in Q1 2021 (low rates + stimulus). It has since risen to 11.3%, crossing above the 10% “stretched” threshold. The driver is not primarily new borrowing but the repricing of existing variable-rate debt at higher rates. Credit card APRs averaging 22.3% for those carrying balances mean even stable balances generate higher required payments. The pre-GFC peak was 15.9%. The DSR has plateaued around 11.1-11.3% for the past two years, but any further rate repricing pushes it higher mechanically.

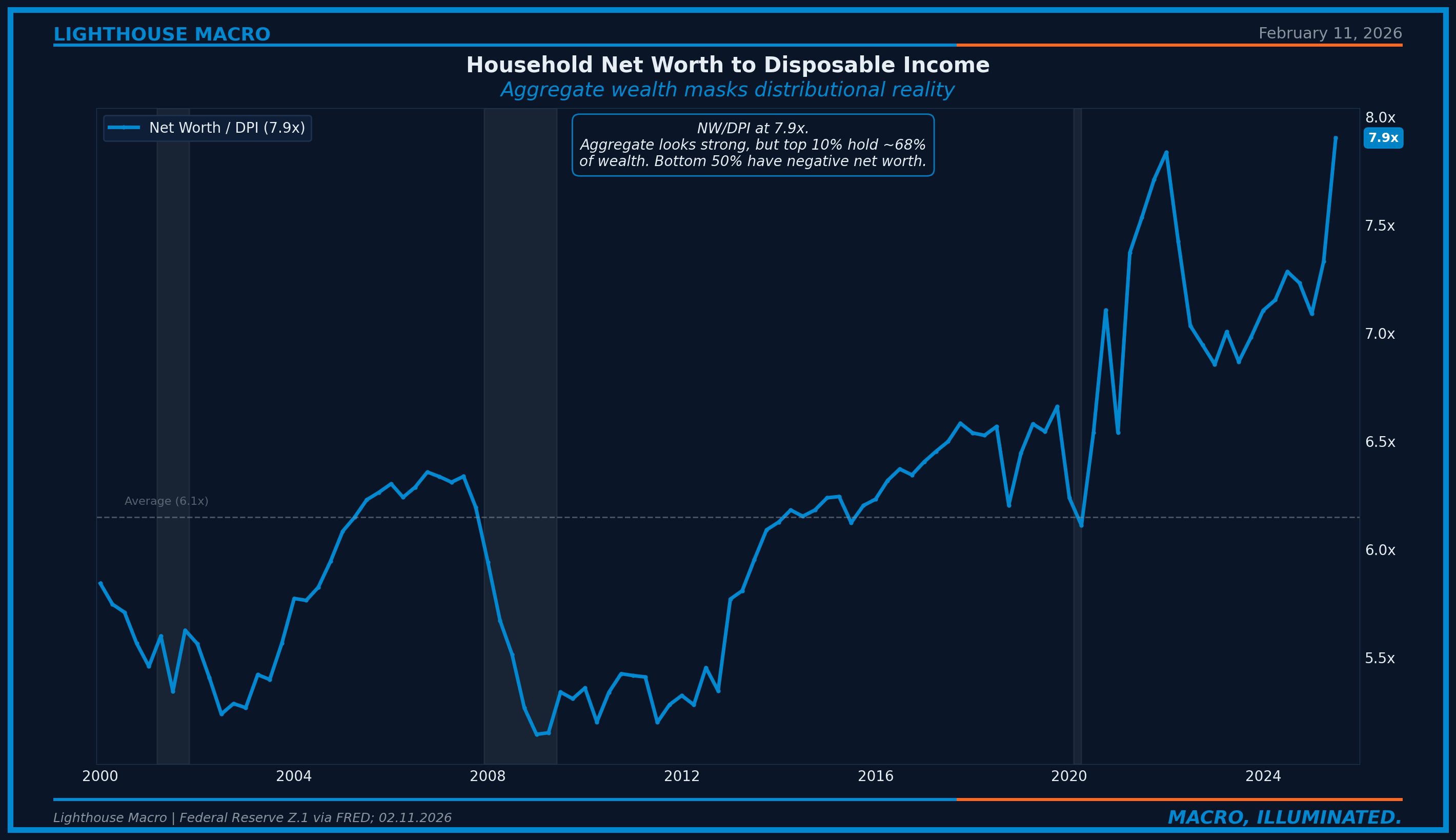

Household Net Worth: The Wealth Mirage

Aggregate household net worth tells one story. The distributional reality tells another.

The NW/DPI ratio at 7.9x (per the Fed’s January 2026 Z.1 update) looks historically strong, above the long-term average of ~6.1x. But the top 10% of households hold roughly 68% of total net worth (Fed Distributional Financial Accounts, January 2026). The bottom 50% hold effectively zero or negative net worth. The “wealthy consumer” is real. The “average consumer” is a statistical fiction. When we say “the consumer is strong” based on aggregate data, we are describing the top quintile.

This bifurcation shows up in spending data. Luxury retailers report robust demand. Discount retailers gain share as middle-income consumers trade down. The aggregate PCE number of +2.6% masks a K-shaped consumer: the top spending +4%, the bottom barely positive or negative in real terms. The “trading down” phenomenon (brand-name to private-label, sit-down to fast-casual, new cars to used) does not show up in the aggregate. But it shows up in corporate earnings: Walmart gains, Target loses. The aggregate holds because the top quintile accounts for roughly 40% of total spending. When even the top pulls back, the aggregate collapses fast.

The Consensus Trap

Here is the pattern that repeats every cycle.

Surface narrative: “Consumer spending is growing 2.6% real. Aggregate payrolls are positive. Net worth is at record highs. The consumer is resilient.”

What is actually happening: Spending is positive but its funding source has shifted from income to credit. The saving rate has collapsed to 3.5%. Credit card delinquencies doubled from their lows, briefly stabilized, then re-accelerated in Q4 2025. Conference Board confidence has plunged to 84.5, the lowest since 2014. The debt service ratio is rising mechanically as variable-rate debt reprices. And the aggregate numbers mask severe bifurcation between wealthy and median consumers.

Consensus gets trapped by three biases.

Aggregation bias. +2.6% PCE can consist of the top quintile at +5% and the bottom at -1%. The average describes an economy that does not exist for most participants.

Lagging bias. Consumer spending is the last domino. By the time PCE contracts, labor has already deteriorated (6-9 months prior), credit stress has built (3-6 months prior), and confidence has collapsed (1-3 months prior). Celebrating “resilient spending” while upstream indicators deteriorate is celebrating a building’s structure while the foundation cracks.

Stock vs flow bias. Net worth at record highs is a stock. The saving rate at 3.5% is a flow. Stocks change slowly. Flows change fast. The depleted saving rate and rising delinquencies are telling you, in real time, that the flow dynamics have already shifted.

Where We Are Now

Applying the framework to current conditions.

The consumer is in Stage 2 of the stress sequence, deeper into it than we assessed even a month ago.

Stage 1 is complete. The excess savings accumulated during COVID (~$2.1 trillion per SF Fed estimates) were fully depleted by Q1 2024. The SF Fed discontinued its savings tracker shortly after. The personal saving rate has fallen to 3.5%, below the 5.5% threshold and now touching the 3.5% “stressed” level that historically precedes spending pullbacks. There is no buffer left.

Stage 2 is accelerating. Credit card delinquencies peaked at ~3.2% in Q2 2024 (highest since 2012) before declining to 3.0% by Q3 2025. The trend appeared to be stabilizing, but the NY Fed’s Q4 2025 Household Debt Report shows aggregate delinquency worsening again to 4.8%, with credit card transitions into serious delinquency ticking higher. Total household debt reached $18.8 trillion. Credit card balances climbed to $1.28 trillion. The improvement was temporary. Revolving credit growing +3.4% YoY. The debt service ratio at 11.3% (above the “stretched” threshold). Credit card APRs averaging 22.3% for those carrying balances. Consumers are borrowing at historically expensive rates to maintain spending. This is inherently unstable.

Stage 3 risk is rising. UMich sentiment has bounced modestly to 57.3 from December’s 53 low, but Conference Board Consumer Confidence collapsed to 84.5 in January, the lowest since May 2014. The Expectations Index at 65.1 is below the 80 threshold that historically signals recession. When consumers feel this pessimistic about the future, spending decisions change. Durables spending is the leading edge. Services will follow if confidence does not recover. December retail sales already came in flat, with the control group at -0.1%. The spending data is starting to confirm what the surveys have been saying.

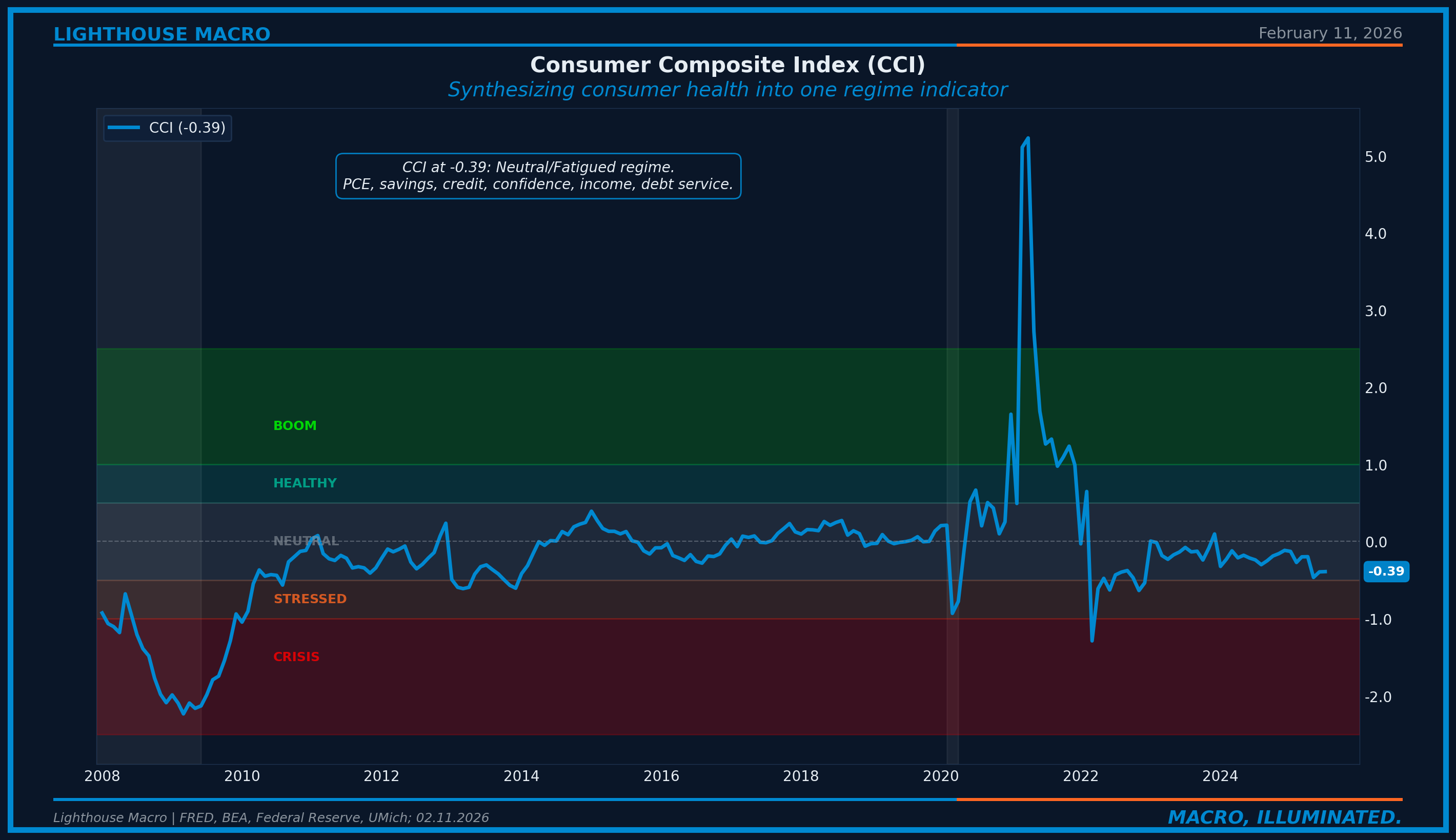

The Composite:

The CCI stands at -0.39 (Neutral/Fatigued), down from +0.7 in December 2019 (Healthy) and +1.8 in April 2021 (Boom, stimulus-fueled). It has descended steadily for over two years. The composite now includes seven components: spending, savings, retail sales, credit, confidence, income, and debt service, with weights validated against forward PCE outcomes. No single indicator is driving the decline. Multiple inputs are moving in the same direction. This is what Stage 2 looks like from the inside: slow, steady erosion that does not make headlines until it is undeniable.

The Cross-Pillar Connection

The consumer does not exist in isolation. It connects to every other pillar in the framework, usually as the receiving end of transmission chains that started elsewhere.

Consumer to Labor: The reinforcing loop. Spending contracts, revenues fall, companies cut hours then headcount, income drops, spending drops further. Current: aggregate payrolls decelerating (+3.7% nominal, +1.1% real). The Labor Fragility Index (LFI) from our first post remains elevated. If CCI continues to deteriorate alongside elevated LFI, the loop activates.

Consumer to Prices: Consumer weakness is disinflationary. When spending slows, pricing power fades. If consumer spending decelerates further, services inflation (the “last mile”) finally resolves. Consumer weakness may be the catalyst that gives the Fed room to cut. The wildcard: tariff pass-through. Businesses absorbed roughly 80% of tariff costs in 2025, but that absorption is projected to shrink to ~20% later in 2026 as the effective tariff rate has risen from 2.1% to ~11.7%. The consumer may face simultaneous income deceleration and price acceleration. That is not a combination the fuel tank can handle.

Consumer to Growth: PCE is 68% of GDP. If consumer spending decelerates from +2.6% to +1.5%, the PCE contribution to GDP falls by ~0.7 percentage points. The consumer is the margin.

Consumer to Housing: With UMich at 57 and Conference Board at 84.5, there is no catalyst for housing demand recovery. Housing and consumer form a reflexive loop: weak consumers cannot buy homes, and a frozen housing market cannot generate the wealth effect that supports confidence.

Consumer to Financial Conditions: If delinquencies continue rising toward 4.5%, banks tighten lending standards, which reduces credit availability, which further constrains spending. The negative feedback loop that turns cyclical weakness into systemic stress. Not there yet. Watching.

How to Track This Pillar

Real PCE YoY. The 68% anchor. Below +1.5% = stagnation. Below 0% = contraction. (Monthly, BEA)

Personal Saving Rate. The fuel gauge. Below 5.5% = stretched. Below 3.5% = stressed. (Monthly, BEA)

Credit Card Delinquency Rate. The early warning. Above 3.5% = stressed. Above 5.0% = crisis. Leads spending cuts by 3-6 months. (Quarterly, Federal Reserve)

UMich Consumer Sentiment. The confidence pulse. Below 80 = weak. Below 65 = recessionary. (Monthly, UMich)

Retail Sales Control Group. The monthly spending check. Strips autos, gas, building materials. Feeds directly into GDP. (Monthly, Census)

Debt Service Ratio. The payment burden. Above 10% = stretched. Above 13% = stressed. (Quarterly, Federal Reserve)

Aggregate Weekly Payrolls YoY. The income reality. Employment times hours times wages. Below 3% nominal = income stagnation. (Monthly, BLS)

Release schedule: UMich prelim and retail sales (mid-month) for first read. PCE and income data (end of month) to confirm. Credit quarterly for stress signals.

Invalidation Criteria

Every thesis needs an exit door.

Bull Case (Consumer Resilience) Confirmation:

If the following occur simultaneously for 3+ months, the consumer stress thesis is invalidated:

Personal Saving Rate rises above 6.0% (buffer rebuilding)

Credit Card Delinquency drops below 2.5% (stress fading)

Real PCE YoY exceeds 3.0% (acceleration)

UMich Sentiment exceeds 80 (confidence recovering)

Real DPI YoY exceeds 2.5% (income growth supporting spending)

CCI exceeds +0.5 (healthy regime)

Current status: Zero of six conditions met. All six are moving in the wrong direction.

Action if confirmed: Rotate to consumer discretionary, travel/leisure, retail. Consumer strength drives cyclical outperformance.

Bear Case (Consumer Collapse) Confirmation:

If the following occur, the consumer is deteriorating beyond stress into crisis:

Real PCE YoY turns negative (spending contraction)

Personal Saving Rate drops below 3.0% (desperation)

Credit Card Delinquency exceeds 4.5% (credit crisis)

UMich Sentiment drops below 50 (deep pessimism)

Retail Sales 3-month average turns negative (demand destruction)

CCI drops below -1.0 (crisis regime)

Action if confirmed: Maximum defensive. Overweight consumer staples, discount retail, utilities. Avoid all discretionary exposure.

Framework drives positioning, but the framework can be wrong. Data determines outcome.

The Bottom Line

The consumer is not a leading indicator. It is the 68% of GDP that confirms what everything else already said.

When quits collapse (6-9 months before), credit stress builds (3-6 months before), and confidence craters (1-3 months before), the consumer eventually follows. By the time retail sales go negative, the recession is already underway. The consumer does not predict. It validates.

The aggregate numbers still look okay. Real PCE at +2.6%. Aggregate payrolls positive. Net worth at record highs. But aggregates mask the funding source shift from income to credit, the distributional reality where the top quintile carries the headline, and the flow dynamics that have already shifted.

Saving rate at 3.5%. Delinquencies re-accelerating after a brief reprieve. UMich at 57 but Conference Board at 84.5, the lowest since 2014. DSR at 11.3%. CCI at -0.39. The consumer has not cracked. But the cracks are deeper than they were, and they are widening. When the last domino falls, everyone will see what the data said months ago.

This is how we analyze the consumer.

Join The Watch.

Bob Sheehan, CFA, CMT

Founder & CIO, Lighthouse Macro

This is the fourth in a 12-part series on the Lighthouse Macro framework. Next up: Housing and the Frozen Equilibrium.

Great research. Thank you for explaining the framework in detail, and helping readers to “connect the dots”.

Great post, learned quite a lot. Thank you