The Fed Put, Retired

The Beacon · June 15, 2026

For fifteen years every selloff was bought on the same faith, that a chair stood behind the tape ready to rescue it. That chair takes his seat Wednesday, and he spent his career arguing against the rescue. The wrinkle is that disinflation is finally showing up, the one thing that usually buys the cut, and we do not think it pays this time.

Markets have a reflex, and like all reflexes it was trained. For fifteen years, through every wobble and every crash, the lesson was the same. When things got ugly enough the Federal Reserve would cut, or flood, or at minimum signal that help was on the way, and the long end would come back down to rescue whatever had broken. Buyers learned to step in ahead of it. The reflex paid often enough that the market stopped asking whether the rescue was actually coming and started treating it as a law of nature.

You can date the lessons. The pivot in early 2019, when the tape broke on too much tightening and the Fed reversed within weeks. The flood in 2020, when the balance sheet nearly doubled in a matter of months. The quiet backstop in the spring of 2023, when a handful of regional banks wobbled and a lending facility appeared almost overnight. Each time the pattern held, and each time it taught the same lesson, that the Fed’s tolerance for market pain was finite and the put was real. A whole generation of investors has never once been positioned against it.

This week the reflex is firing again, quietly, in the way investors lean on a dovish pivot the moment a print softens. And it runs straight into a problem the tape has not priced. The man who breaks the tie at the June 16 and 17 meeting is Kevin Warsh, and the rescue is the exact thing he has spent his career arguing the Fed should stop providing.

So here is the claim, stated plainly so you can hold us to it. The market is pricing a Fed put that is being retired in real time, and the disinflation now arriving will not buy it back. We will show our work on real data, the kind anyone can pull and check. If credit starts pricing stress, if the long end rolls over, and if the new chair blinks dovish on Wednesday, we are wrong and we will say so. None of those is happening yet.

The Reflex Is Firing Into a Calm Tape

Start by being honest about what this is and what it is not. This is not a crash call. It is not even a selloff call anymore. The scare that rattled the headlines a couple of weeks ago has already been bought. The S&P closed today around 7,554, back near its highs. Small caps led the recovery, the Russell up better than four percent on the week. More than sixty percent of the index sits above its 200-day average, the broad tape is healthy, and volatility has bled back down to a 16 handle after touching 21 when the worry was fresh. The dip got bought, exactly the way fifteen years of training said it would.

That texture is the tell, because it tells you what the reflex just did and what it now assumes. It worked. Weakness showed up, buyers stepped in ahead of the rescue, and the tape is back at the highs wearing a 16 vol. The bet underneath a thousand screens is no longer to buy this dip. It is the quieter, more dangerous one. That the next dip gets bought too, because the backstop is still there.

We think that bet is leaning on a backstop that is being dismantled. The tape is calm enough that the interesting question has nothing to do with whether something is breaking. The question is whether the thing everyone is counting on to catch the next break still exists.

The Referee Takes His Seat

Kevin Warsh was sworn in on May 22. There has been no policy meeting since Jerome Powell’s last on April 29, so this week is unambiguously his first in the chair. The decision itself is a formality. A hold at 3.50 to 3.75 percent is priced at something like ninety-nine percent, and we can move past it. The meeting matters for everything around the decision. The projections, the dot plot or whether he keeps one at all, the language on whether an easing bias survives, the tone on the balance sheet, the cadence he sets at the podium. Those are the tells, and every one of them points the same way.

He inherits a divided committee. The April meeting produced an 8-to-4 vote, the most dissents at a single FOMC since 1992, with some members wanting a cut and others objecting to an easing bias sitting in the statement at all. Warsh inherits that split, and on the public record he lands with the hawks. He has argued for years for a smaller balance sheet, for a Fed that holds less duration, for sound money, and against the reflexive accommodation that defined the prior regime. We want to be careful and call that what it is, his stated views and the market’s reasonable reading of them, which is a different thing from announced policy or a meeting outcome.

Watch the projections in particular. The prior dot plot still carried a cut or two penciled in for this year. If the median loses them, or if the committee sketches a hike, that is the market’s signal to flip from pricing easing to pricing its opposite, and it would land on a tape still leaning the old way. Watch whether the easing-bias language survives at all. And watch whether Warsh treats the dot plot as an institution worth keeping or signals he would rather scrap it, because a chair who distrusts forward guidance is a chair telling you not to count on a telegraphed rescue.

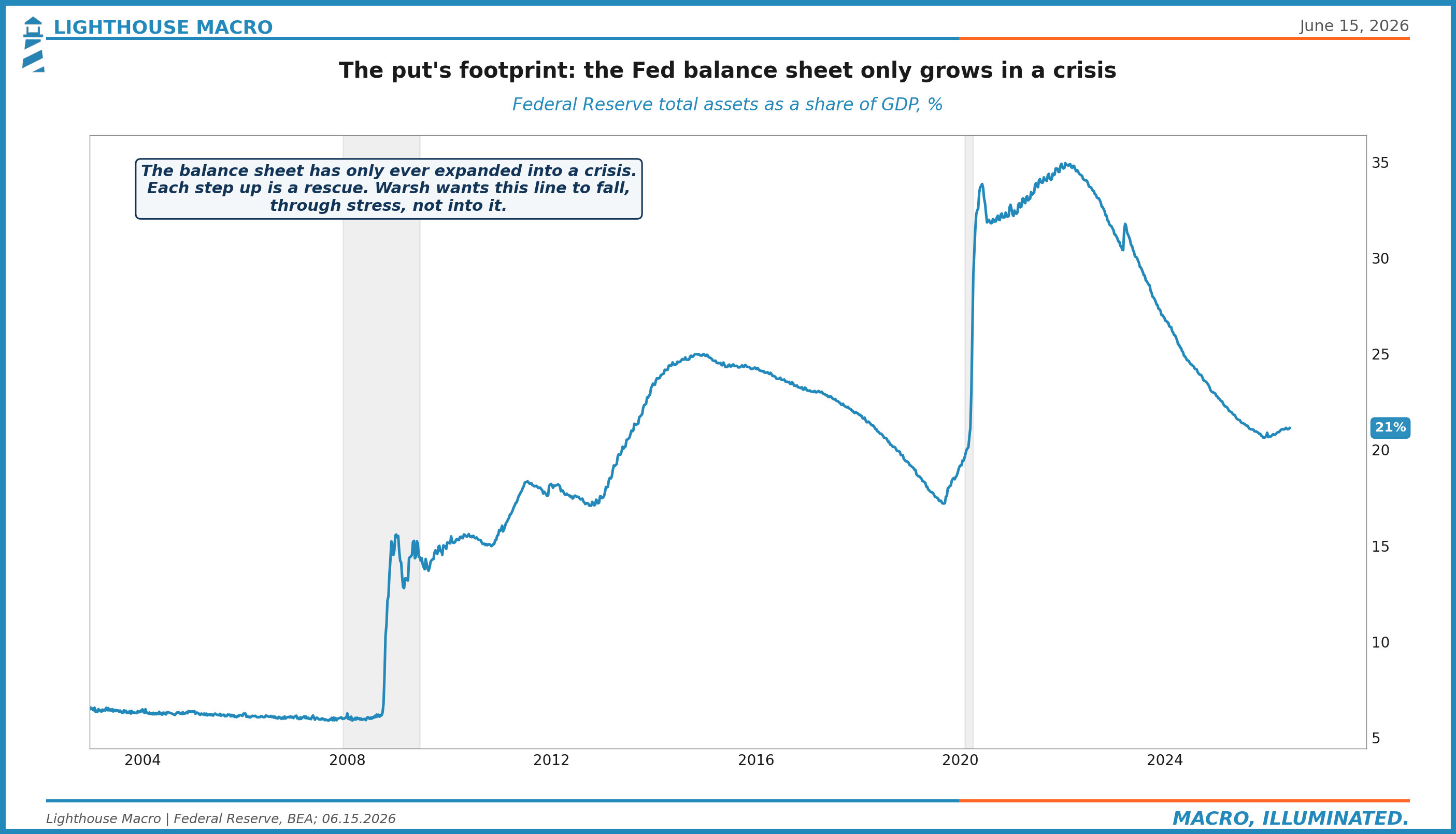

Look at what he is taking over. The Fed’s balance sheet ballooned in every crisis of the last two decades, each expansion a rescue, and even after two years of slow shrinking it still dwarfs anything seen before 2008. A chair who has argued for years to shrink it further wants to retract the most visible arm of the put. The reflex assumes the balance sheet rides in again the moment things break. He has spent his career arguing it should not, and on Wednesday he sets the agenda.

The Engine He Wants More Of

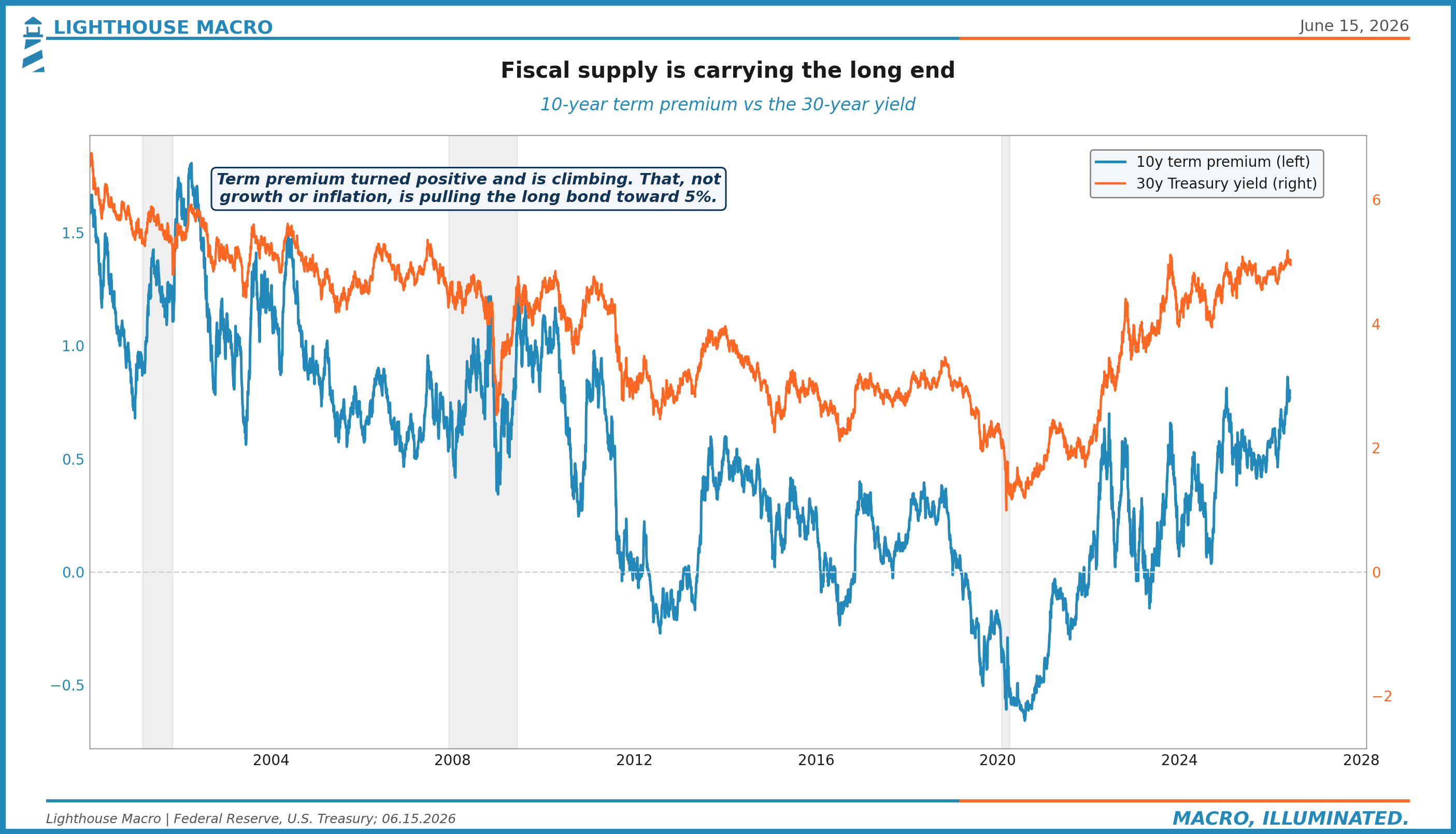

The reason the long end refuses to come down has nothing to do with growth or next month’s inflation print. It is supply, plain and simple. The government is funding enormous deficits, the market is being asked to hold a mountain of long-dated paper, and it is demanding to be paid for the privilege. That premium, the extra yield investors require to hold a long bond rather than roll short ones, has gone from deeply negative to clearly positive over the last two years and keeps grinding higher.

That is the engine pulling the 30-year toward five percent. Read it against what Warsh wants and the implication is uncomfortable. The force already lifting the long end is the force the new chair would rather lean into than fight. A Fed that wants less duration on its balance sheet and a steeper curve is a Fed comfortable with a higher long end. The rescue the reflex is pricing runs directly against the chair’s own stated preference.

And this is not a passing technical that fades when sentiment improves. The deficits are structural, the issuance calendar is relentless, and there is no obvious marginal buyer stepping in to fund it cheaply now that the Fed is shrinking its own holdings rather than adding to them. The premium is simply the market’s price for that imbalance, and it does not melt away on one soft inflation print.

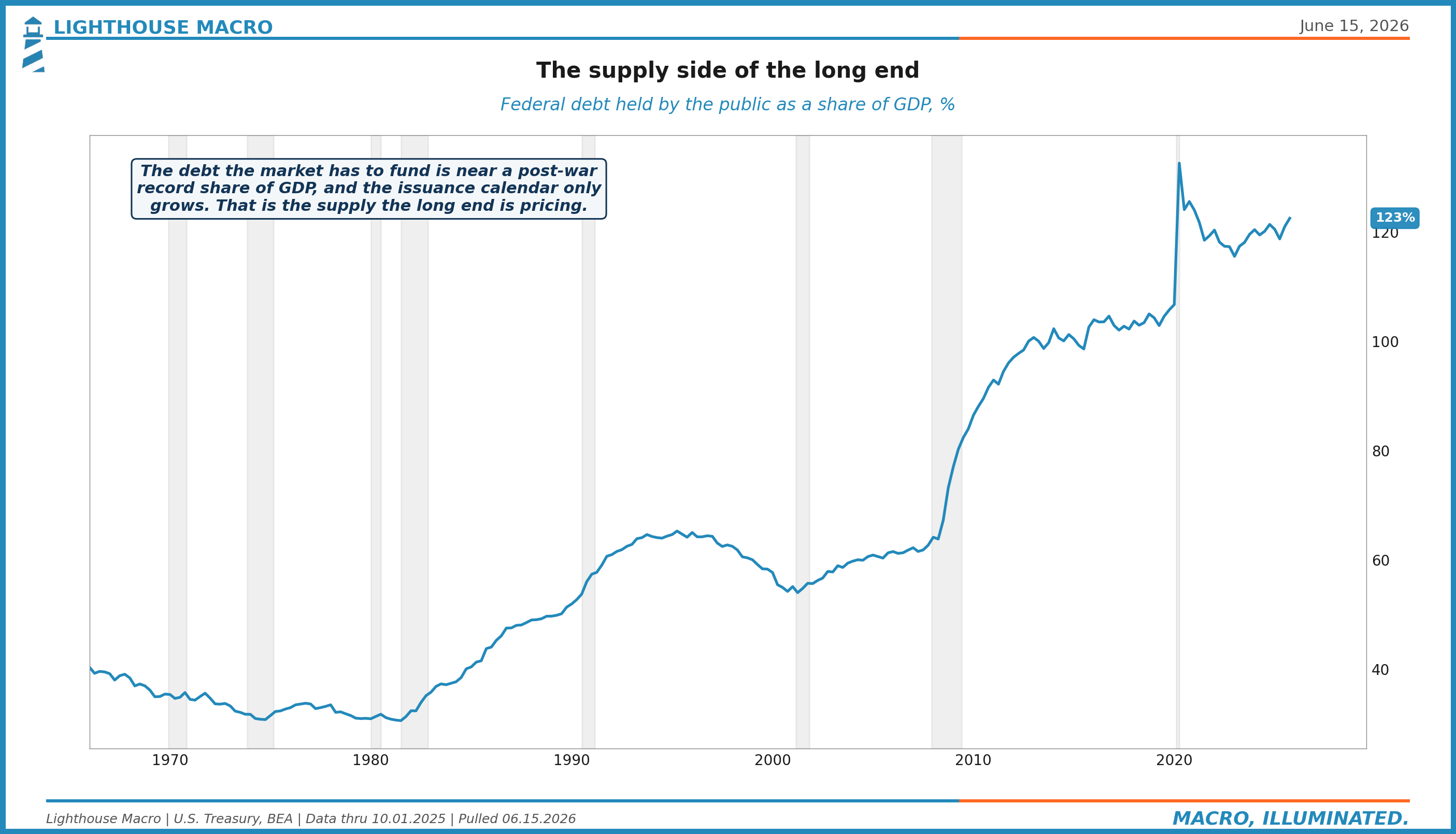

The scale is the point. Federal debt held by the public sits near a post-war record as a share of the economy, and the deficits that feed it are structural rather than cyclical. Someone has to absorb every new auction, and the price of absorbing it is the premium you read off the long end.

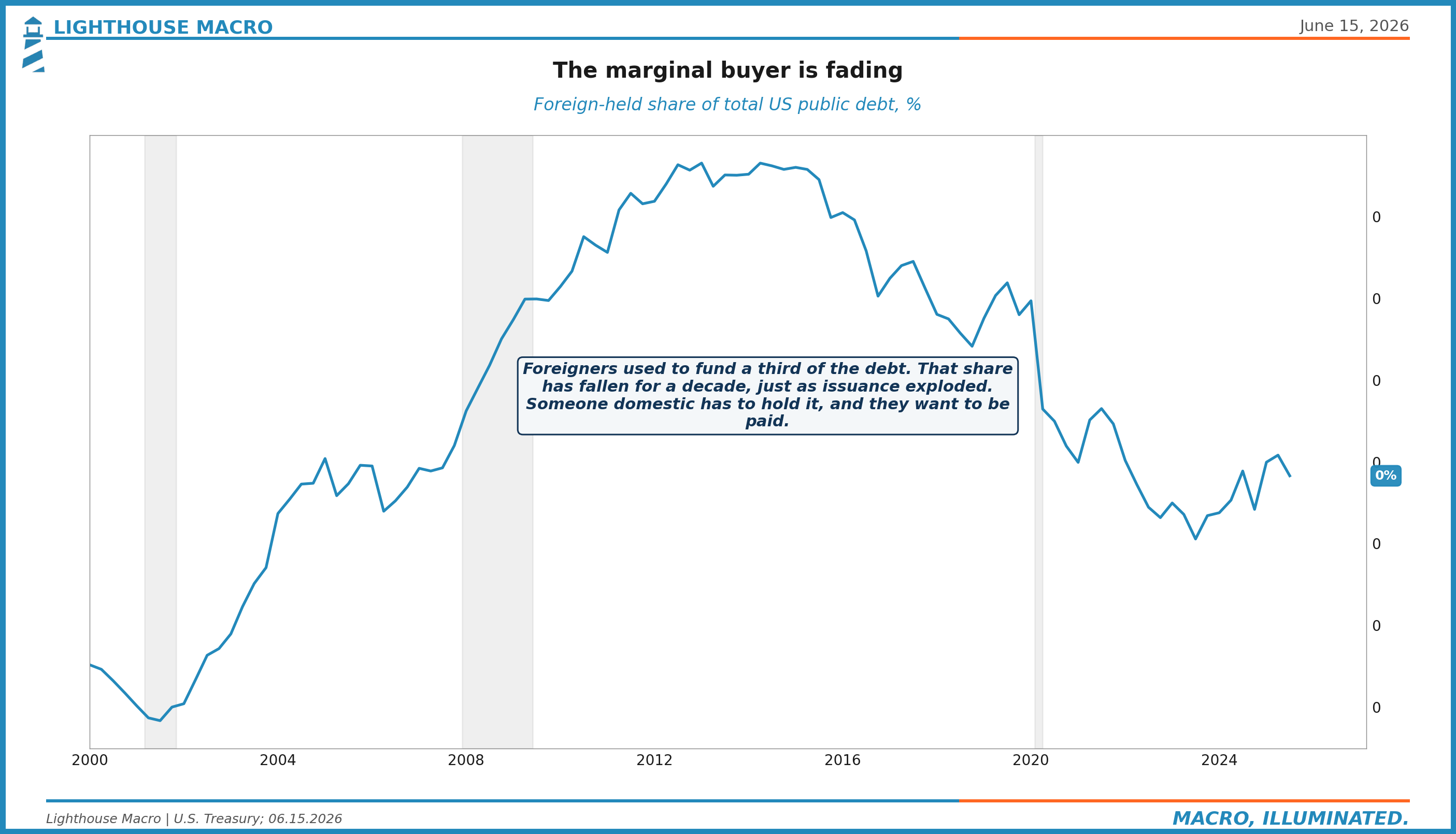

For years that someone was foreign. Overseas official buyers once funded close to a third of the debt, and that share has fallen for a decade even as issuance exploded. The marginal buyer now is domestic and price-sensitive, and a price-sensitive buyer demands to be paid.

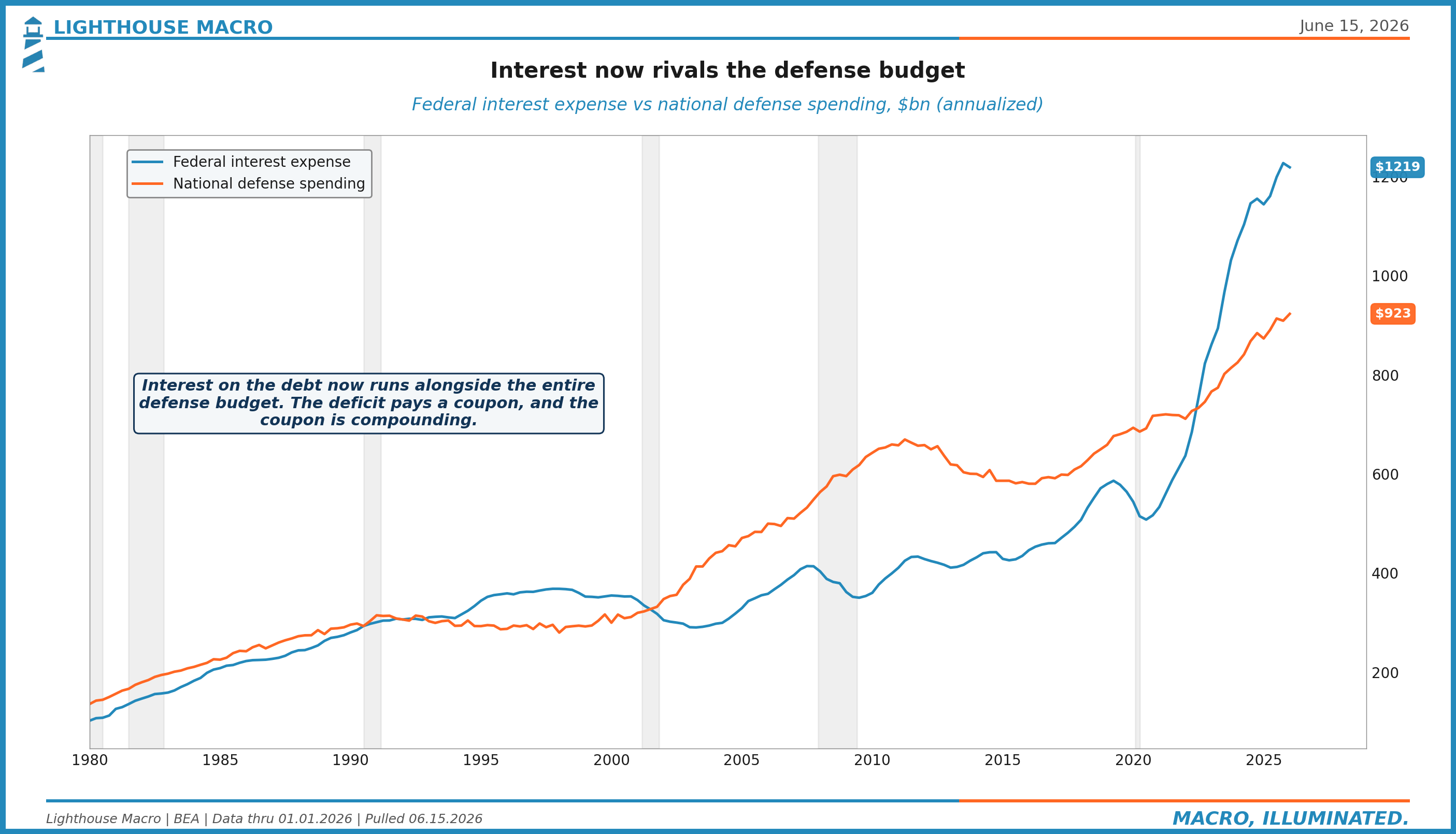

And the cost of carrying the pile compounds. Federal interest expense now runs alongside the entire national defense budget, and every basis point the long end rises makes next year’s deficit worse, which means more issuance, which means more premium. That loop is the engine, and it does not care what core inflation printed last month.

Now decompose the move, because the inflation read is the one most likely to be gotten backwards here. Split the 10-year into its two pieces, the real yield and the inflation compensation buried inside it, and the story is clear. The real yield sits near the high end of its fifteen-year range while the market’s inflation expectation has drifted lower, down toward 2.3 percent. Real is doing the work. The bond market is demanding more yield because the real cost of money is rising and because someone has to be paid to absorb the supply. The long end is high because of who has to fund the government and at what price, and a soft inflation print does nothing to change that. So the usual rescue logic, that cooler inflation lets the Fed ease the long end back down, misfires at the source.

Disinflation Arrives, and the Rescue Still Doesn’t

Here is the part that should, on paper, hand the dip-buyers their catalyst. The disinflation they have been waiting for is actually showing up.

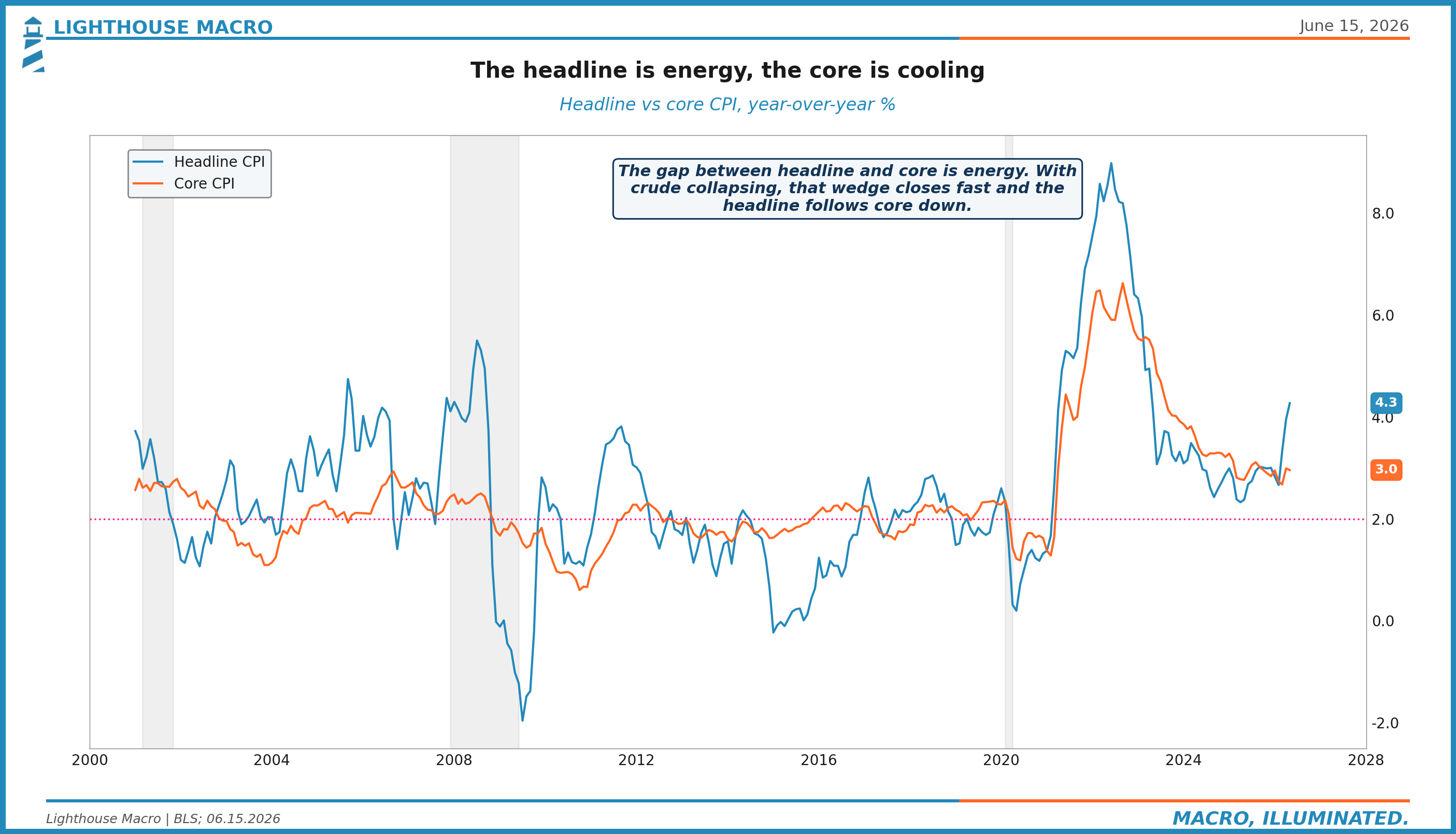

May CPI was a hot headline on a soft core. The headline ran 4.2 percent over the year, dragged up by energy at 6.7 percent on the month and gasoline at 8.6 percent, the last echo of an oil scare that has run since February. But the core, the part the Fed actually steers by, came in soft, up two tenths on the month and 2.8 percent over the year, with shelter cooling. Strip the energy and the disinflation is doing exactly what a patient committee would want to see.

The gap between that hot headline and that soft core is energy, and energy just broke.

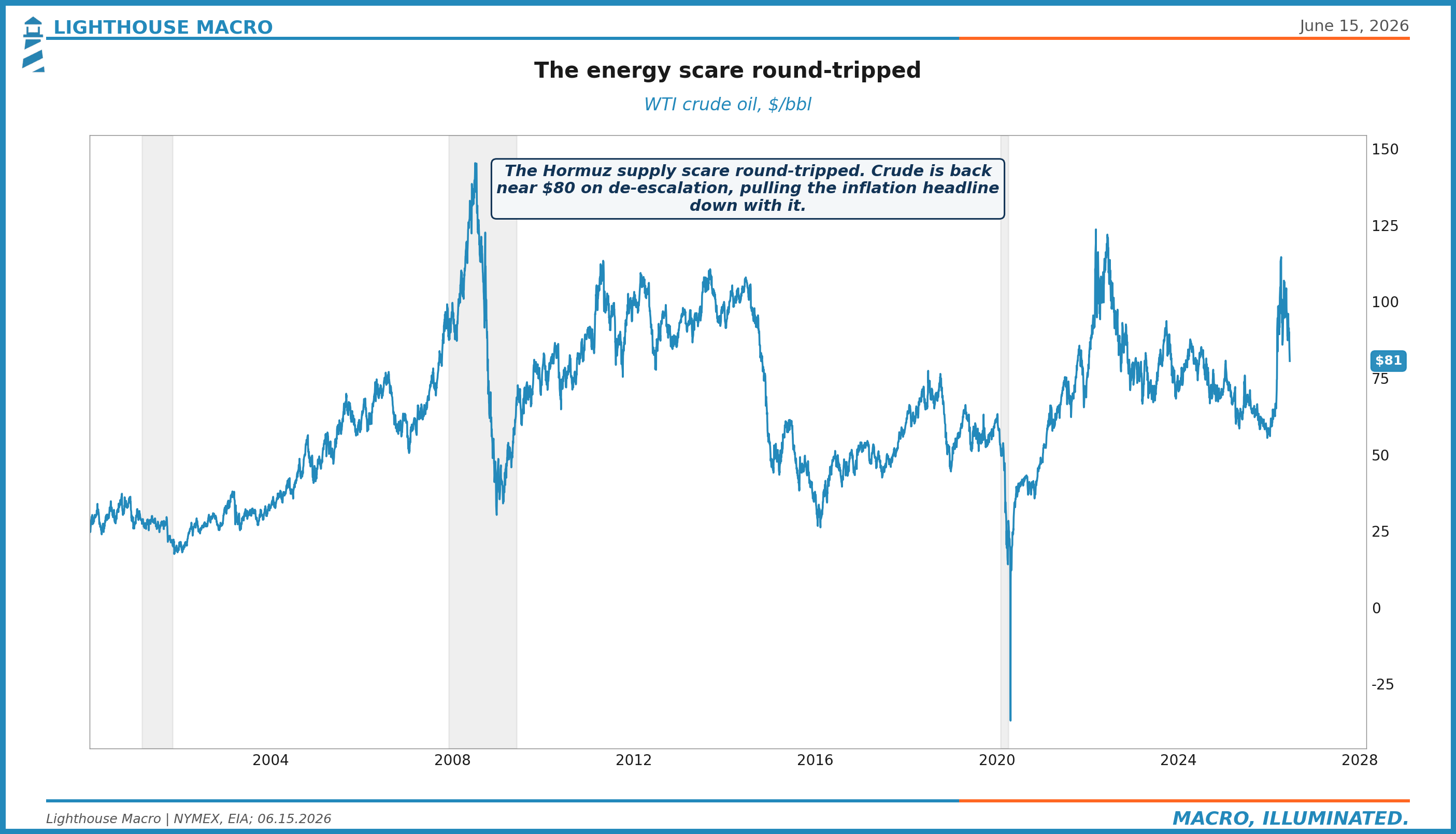

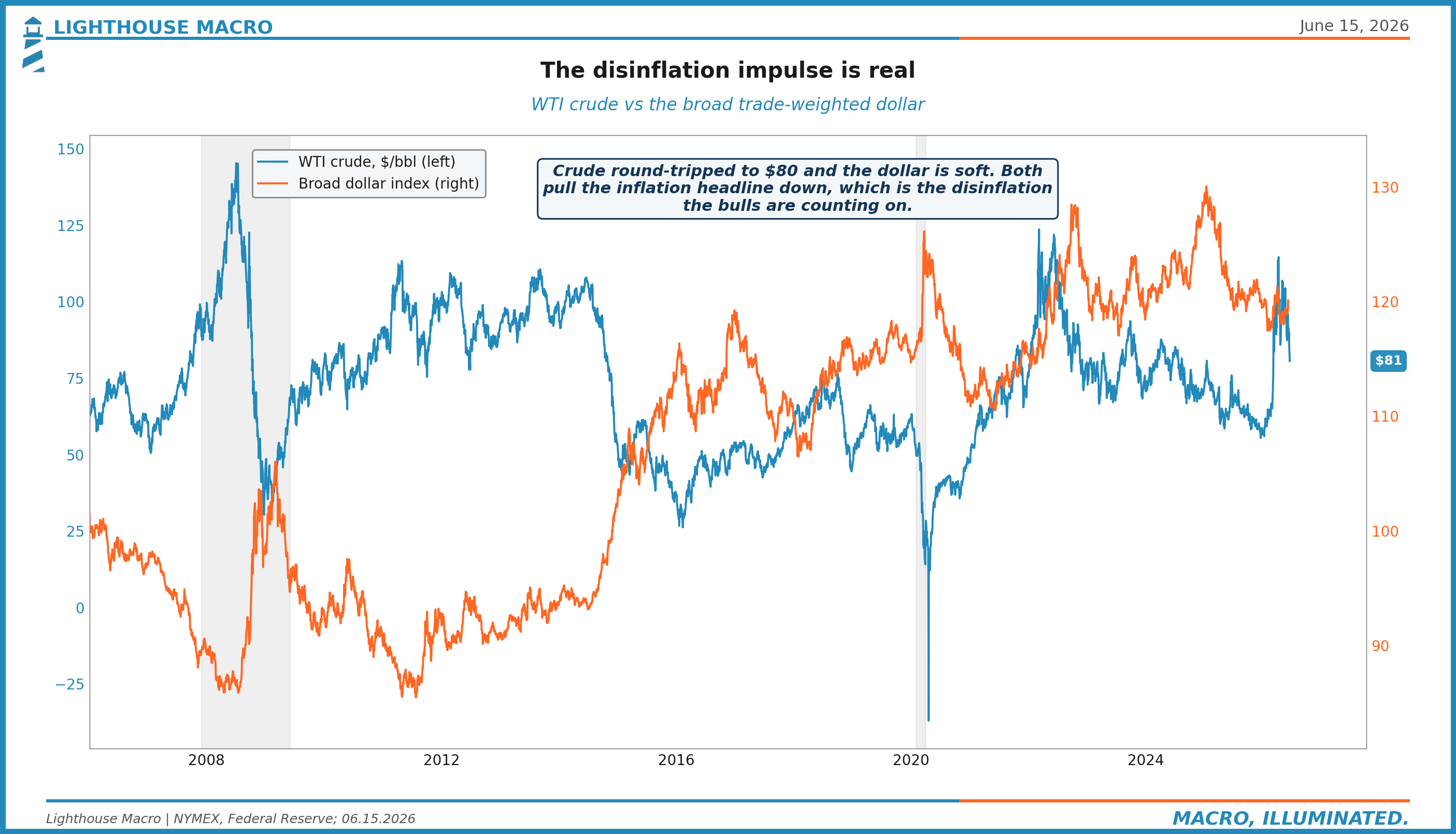

Crude round-tripped the entire war premium. Over the past week front-month WTI collapsed about fourteen percent to roughly 80 dollars, an eight-week low, as hopes built around a US-Iran interim deal that would lift oil sanctions and reopen the Strait of Hormuz. The dollar is soft alongside it. Both work to pull the headline down toward the core, which is the direction that takes pressure off prices.

So put it together. A soft core, a collapsing energy headline, a soft dollar, inflation expectations drifting lower. A normal Fed eases into this. That is the trap in the bull case, and it is a good trap, because the disinflation is genuine. But walk it through. The thing keeping the long end elevated was never the front-end inflation story. It is the supply premium, the cost of duration in a world of relentless issuance. So the very disinflation that should green-light a rescue does almost nothing for the 30-year, and a chair who wants more term premium has no reason to manufacture one. The excuse arrives. The rescue does not follow it. That is the whole piece in three sentences.

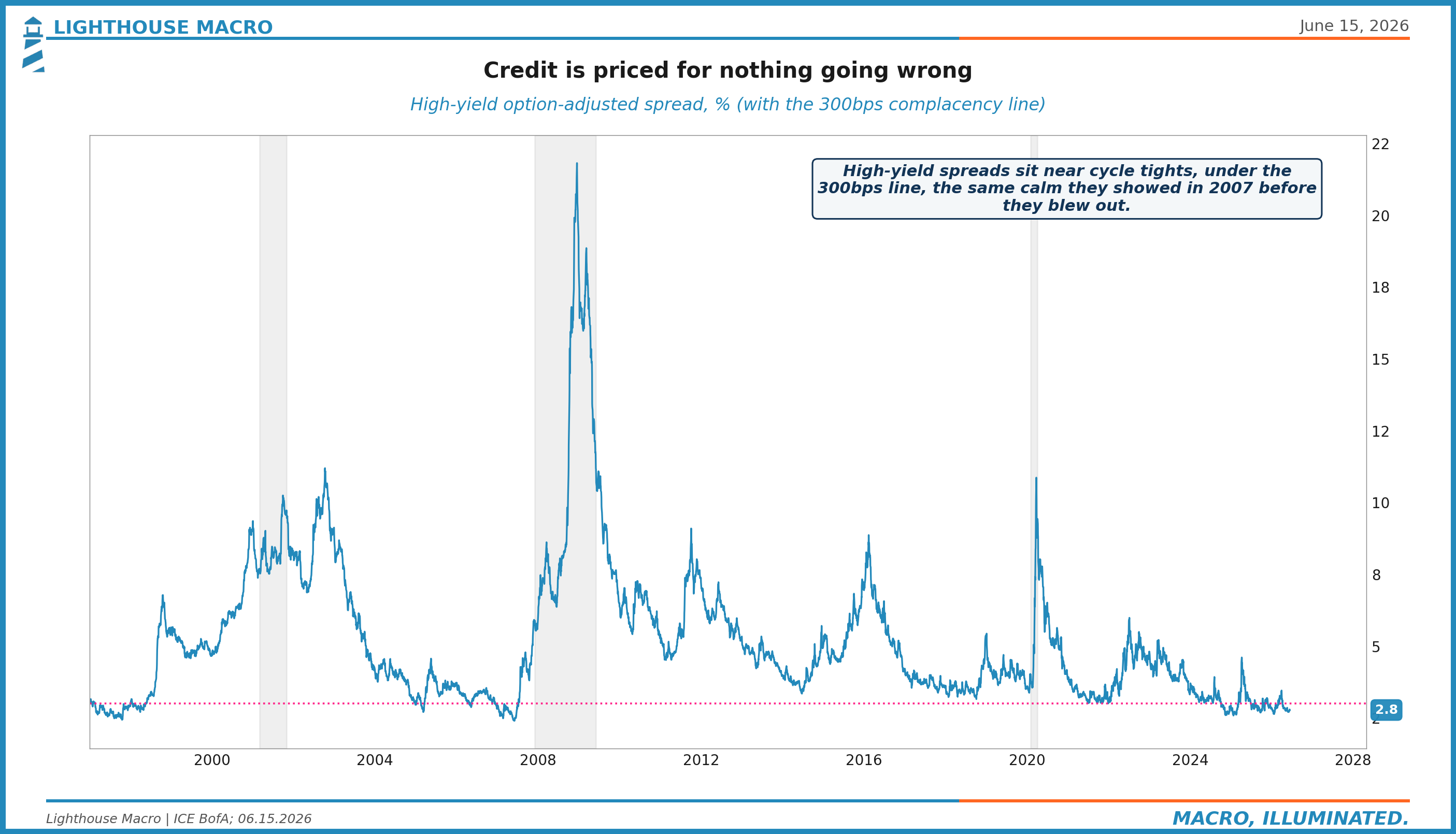

Credit Isn’t Pricing a Rescue Either

If something were actually breaking, the part of the market whose entire job is to price default risk would be the first to say so. It is silent, and the silence cuts against the reflex from the other side.

High-yield spreads sit near 2.8 percent, investment grade near 0.75 percent, both close to the tightest levels of the cycle and well under the 300 basis point line where credit even begins to register concern. Equities took a real scare a couple of weeks ago and then ripped all the way back, and through both moves these spreads barely twitched. Pull the chart back far enough and the discomfort is obvious. This is the same flavor of calm credit wore in 2007, camped out at the tights deep into the year, looking fine right up until it was not, and then gapping rather than drifting when it finally moved.

There is a reason the tightest part of the credit market makes the least reliable warning. Spreads compress when capital is plentiful and reaching for yield, which is precisely the late-cycle condition that tends to precede the turn. The blow-outs in 2008 and 2020 did not build slowly off wide levels. They detonated off tight ones. The equity reflex treats spreads this tight as an all-clear. We read them as the absence of a cushion, the market pricing perfection into a regime that is busy removing the backstop perfection was leaning on. We are not calling a credit blow-up here, and we want to be precise about that. We are making the narrower point that spreads this compressed leave no room for error if the rescue everyone is pricing turns out not to come.

What It Means If You Borrow

If you do not trade a single share, this section is for you, and it carries the same weight as everything above it. To an operator, the rescue the market is pricing is concrete. It is the cut you were counting on, the refinance you were waiting to get cheaper, the rate you penciled into next year’s plan.

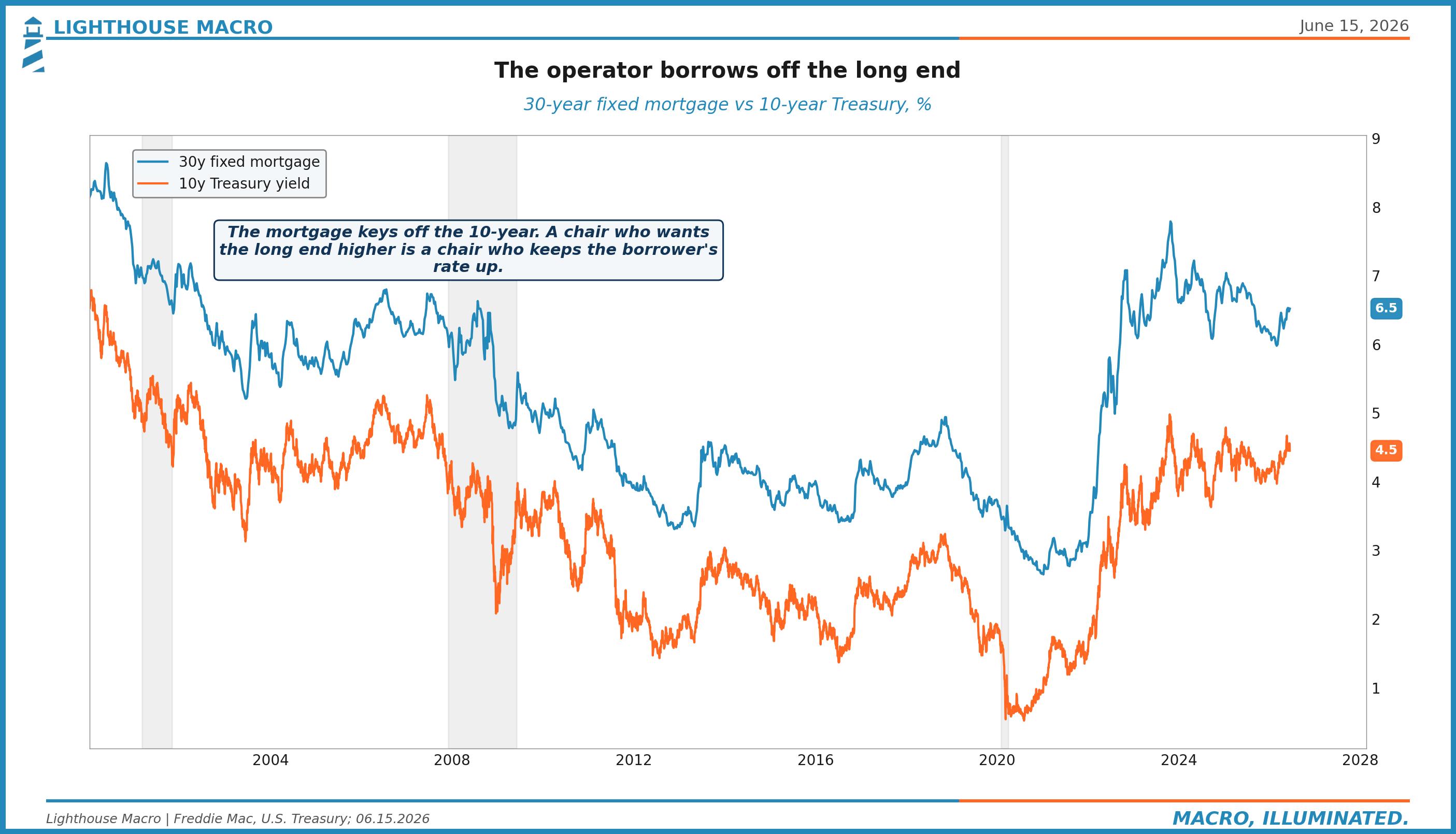

Watch how the cost of long money actually reaches you. The 30-year fixed mortgage sits at 6.52 percent because it keys off the 10-year Treasury yield, and the 10-year is the very thing a steeper-curve chair wants higher rather than lower. There is no separate dial the Fed turns to bring your borrowing cost down while it holds the long end up. They are the same dial. A chair comfortable with a high long end is a chair comfortable with your mortgage, your maturity wall, and your line of credit staying expensive.

This is the split we keep coming back to. There is the economy that owns the assets, that watched the index hold near its highs and felt fine, and there is the economy that borrows to operate, that lives on the price of credit and feels every basis point of it. The first economy is debating whether to buy the dip. The second is deciding whether to break ground, refinance a building, or roll a line of credit into a long end that refuses to come down. A retired Fed put is a footnote to the first economy and a regime change to the second.

The places it bites first are predictable. Commercial real estate has a wall of maturities coming due that was underwritten when money was cheap and now has to refinance into rates that are not. Small businesses run on floating-rate credit that prices off a short rate the chair intends to hold firm. Private portfolios carry floating debt that a rescue cut was supposed to relieve. None of those borrowers got the memo that the backstop is being pulled, and Wednesday is where the memo gets sent.

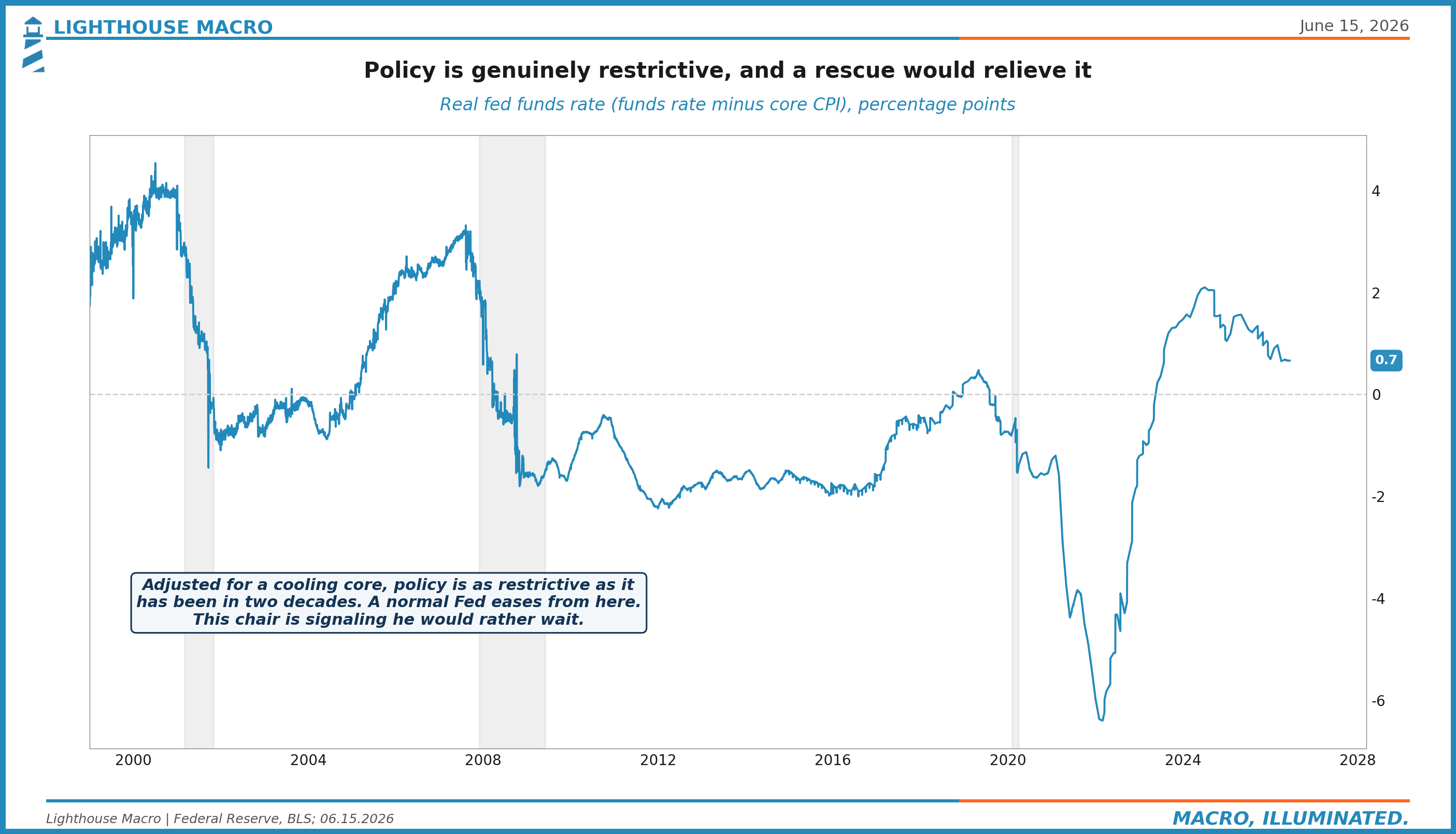

And the cushion most operators assume is there, a Fed that cuts the moment the economy softens, is the very thing in question. Policy is still restrictive against an inflation rate that is cooling.

A normal Fed, looking at a core running under three percent and falling, would already be easing. This one is signaling it would rather wait, and that tells you something about the regime. The bar to a rescue is higher than it has been in a generation.

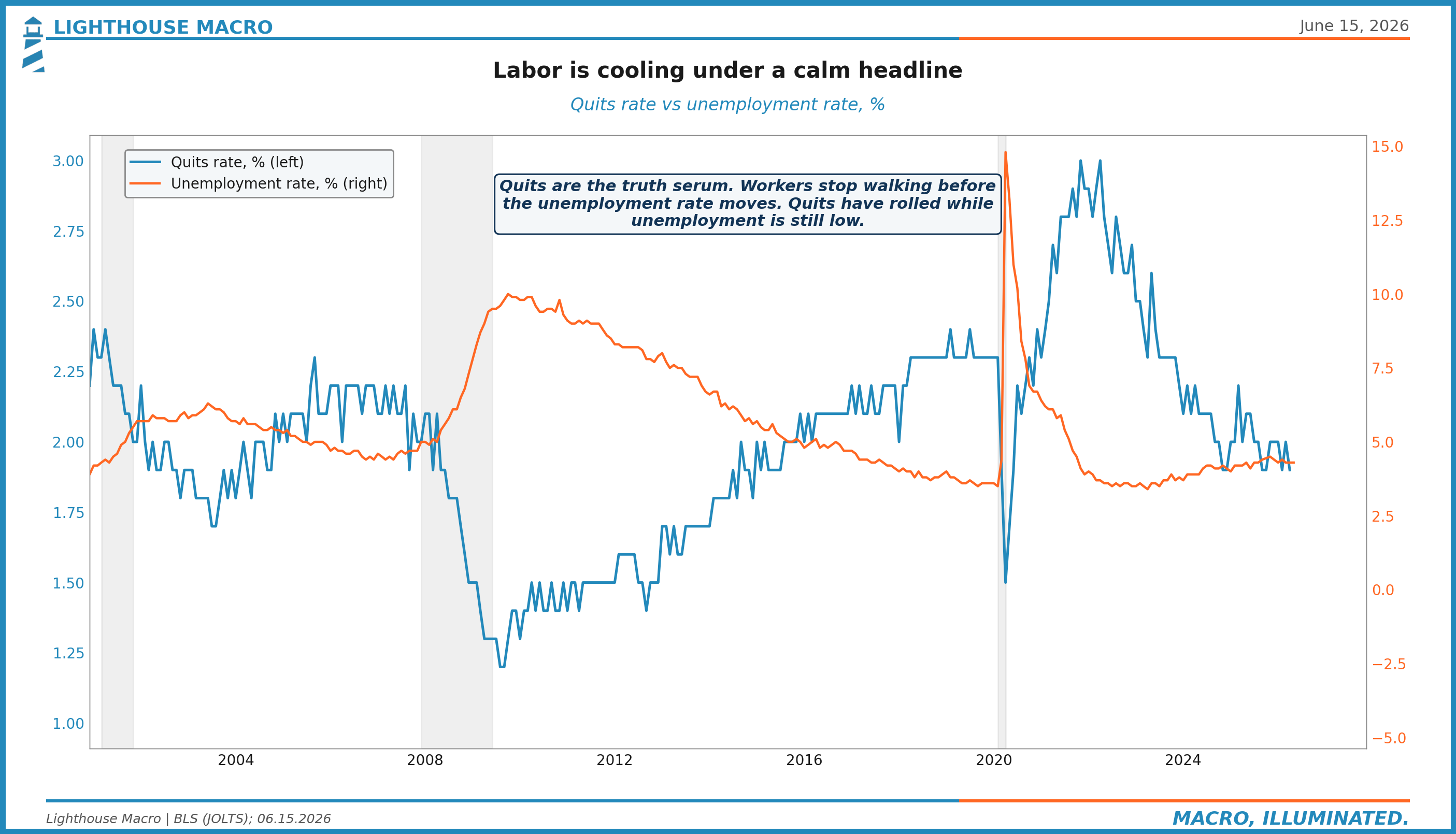

The labor market is the tell to watch, and it is cooling under a calm headline. Quits are the truth serum here. Workers stop volunteering to leave well before the unemployment rate moves, and quits have rolled over while unemployment stays low. By the time the jobs number cracks, the decision is already behind you. So read Wednesday’s projections the way a borrower should, as the clearest twelve-month signal you will get on the price of money. If the dots drift toward no cuts, or toward a hike, plan as if the short end stays high and the long end does not come to you. Finance against the rate you can actually get today, not the one you were hoping a rescue would deliver.

What Would Change Our Mind

We hold a view, so we will tell you plainly what breaks it, because a thesis without an off-switch is just a position you have married.

We are wrong, and the rescue is closer than we think, if three things turn. Credit starts pricing risk, with high-yield spreads widening off these tights instead of sleeping through the tape. The long end rolls over, with the real yield coming down and the supply premium releasing rather than building. And the chair himself blinks, with a dot plot that pencils in more cuts than the last one, or an easing bias kept and reinforced, or a press conference that leans dovish. Any genuine move on that list and we re-risk without apology. Right now not one of them is in motion.

Short of that, the setup is what it is. The reflex to buy weakness is leaning on a backstop that the man taking the chair on Wednesday has spent his career arguing against, and the disinflation that would normally force his hand lands on the front of the curve while the long end stays a fiscal story he is content to leave alone. For investors, that makes the dovish pivot the low-probability bet rather than the base case, and it makes the dot plot and the bias language the highest-leverage things to watch this week, well above the rate decision itself. For everyone whose plans run on the cost of money rather than the level of the index, it means the same thing in plainer terms. The cut you were waiting on is no longer the base case.

The reflex was trained over fifteen years. The trainer just left the building. We find out on Wednesday whether the market has noticed.

That’s our view from the Watch. We’ll keep the light on...

Bob Sheehan, CFA, CMT

Founder & Macro Strategist

Sharpest articulation of the supply-vs-front-end split I've read. One push on the credit section, because the trigger you're waiting for "credit starts pricing risk" is arguably already firing, just not in the venue that prints daily.

HY OAS at 2.71% is the calmest tape in the complex, but it's a bond-market average that doesn't see the floating-rate underbelly your borrower section is really about. Leveraged-loan default rates are running near 7%, roughly double their long-run average exactly where a held-high short end bites first. And the vehicles built on that paper are already rationing exits: BCRED capped Q2 at its 5% gate against ~10% of NAV requested, Partners Group at 5% against 9.8%, Cliffwater at 17%, with Partners flagging it spreading into PE.

That's the sequencing. Internally-marked, gateable credit reprices first and quietly; public HY reprices last because it trades on a screen. So the 2007 calm isn't evidence against the thesis it's what you'd see right before it. Tomorrow sets the regime; the gate is the tell that it's already transmitting.