POSITIONING UPDATE: FEBRUARY 23, 2026

The Tariff Regime Breaks. The Defensive Thesis Doesn’t.

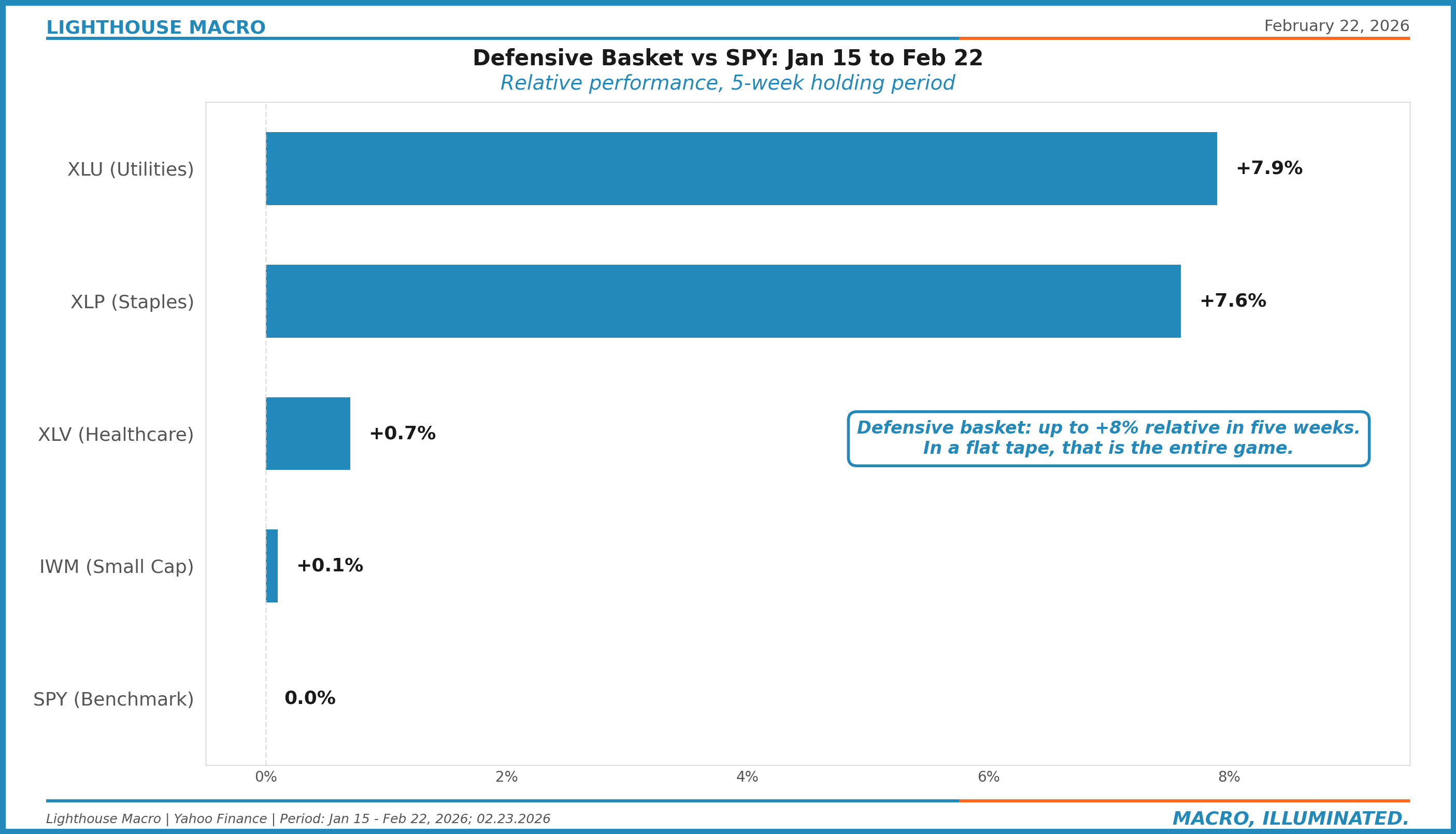

HOW ARE WE DOING: JANUARY 15 TO TODAY

On January 15, we published “Playing Defense in a Hollow Rally.” Our macro risk assessment was elevated. We called for underweighting equities, overweighting defensives, avoiding the long bond, and said VIX in the mid-teens was complacent.

Here is what happened:

Defensive basket vs. SPY: XLU +7.9% and XLP +7.6% relative in five weeks. IWM and XLV flat. The calls that worked, worked big.

The outperformance is not flashy. It is structural. SPY lost 0.6% while XLU returned +7.3% and XLP gained +7.0% absolute. In a flat-to-down tape, that is the entire game.

The vol call is worth highlighting separately. We said VIX in the mid-teens was mispricing risk. VIX moved from 15.44 to 19.09, a 23.6% increase in the index level. The specific P&L depends on expression (VIX calls, put spreads on SPY, long VXX), but the directional read was correct and well-timed.

Four of six legs clearly working (SPY underweight, XLP, XLU, vol). IWM and XLV essentially flat. Credit underweight structurally intact but early. The SCOTUS relief rally does not break any of these calls.

A note on tracking: these are research calls published with timestamps, not a managed portfolio. The piece went out after the close on Jan 15. Prices are sourced from Jan 16 open and Feb 20 market closes. We are building a formal model portfolio with verifiable execution timestamps for future updates. For now, the published calls with dates serve as the audit trail. We would rather show you exactly what we said and when than fabricate a backtest.

WHAT’S IN THIS UPDATE

Labor: The quits rate is sitting on the exact threshold that preceded the last three recessions. The question is not whether the labor market is weakening. It is whether the headline data catches up before or after credit does.

Credit: The gap between what credit is pricing and what the quits rate, openings data, and payroll revisions are saying has not been this wide in over two years.

Plumbing: The shock absorber is gone. RRP is effectively zero. SOFR-EFFR is quiet, but the margin for error just got thinner.

Rates: The steepener is building. Term premium is repricing for a post-QT, deficit-heavy world. The SCOTUS ruling does not change that.

Full analysis: updated macro assessment across labor, credit, plumbing, and market structure. Two Books positioning with entry/exit levels, Technical Overlay watchlist, and explicit invalidation criteria for both directions.