Markets Turn in Order, and the Order Is Almost Done

The Horizon · June 2026

The yield back-up is real and it is fiscal, not a price scare, and that one fact sorts the whole tape. The leaders flashed for weeks. The laggards are catching down on schedule. Two June catalysts, a CPI print and Kevin Warsh’s first meeting in the chair, both cut the same way. The book is built for exactly that.

The Setup: One Fact Sorts Everything

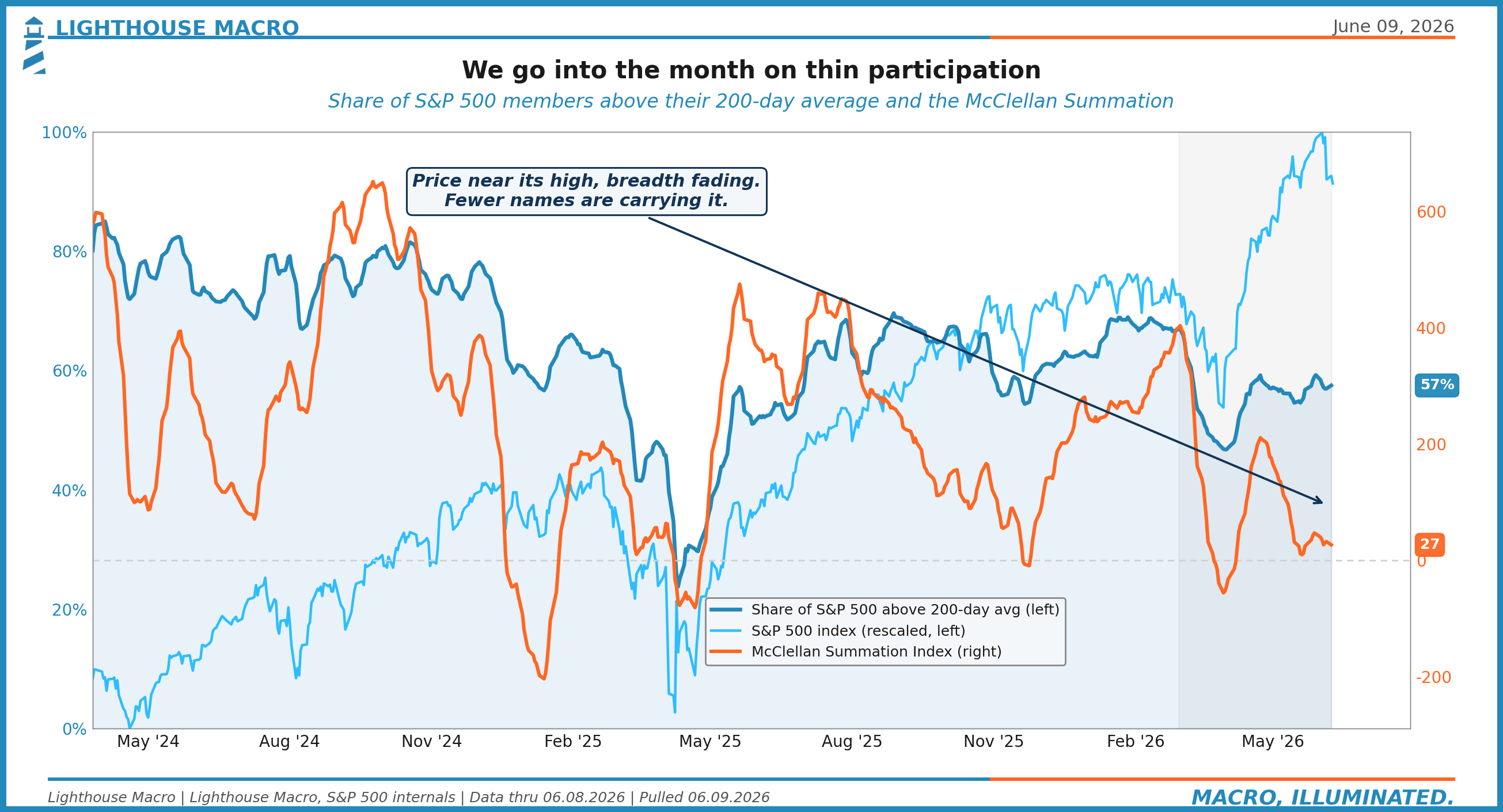

A month ago the question was whether the leaders were right. They were. Breadth thinned while the index made new highs, the term premium ground higher, and the real 10-year backed up toward the high end of its decade-and-a-half range. We told you the tape was turning in order, leaders first, and that the followers had not gotten the message yet.

This is the follow-up, and the message is starting to land. Friday’s payroll cracked the calm. The index wobbled off its highs, the VIX popped to a 20-handle, and megacap tech rolled a second leg lower after a one-day bounce. Then the very next session it steadied, which is exactly how a tape that is rolling rather than breaking behaves. Step back and the picture is clear enough. The S&P is still up high-single-digits on the year and sitting a few percent off its all-time high, carried by a shrinking handful of names, while the leading indicators underneath it have been deteriorating for weeks. The leaders are still leading. The laggards are still lagging. The gap between them is the trade, and over the next month we think it resolves toward the leaders.

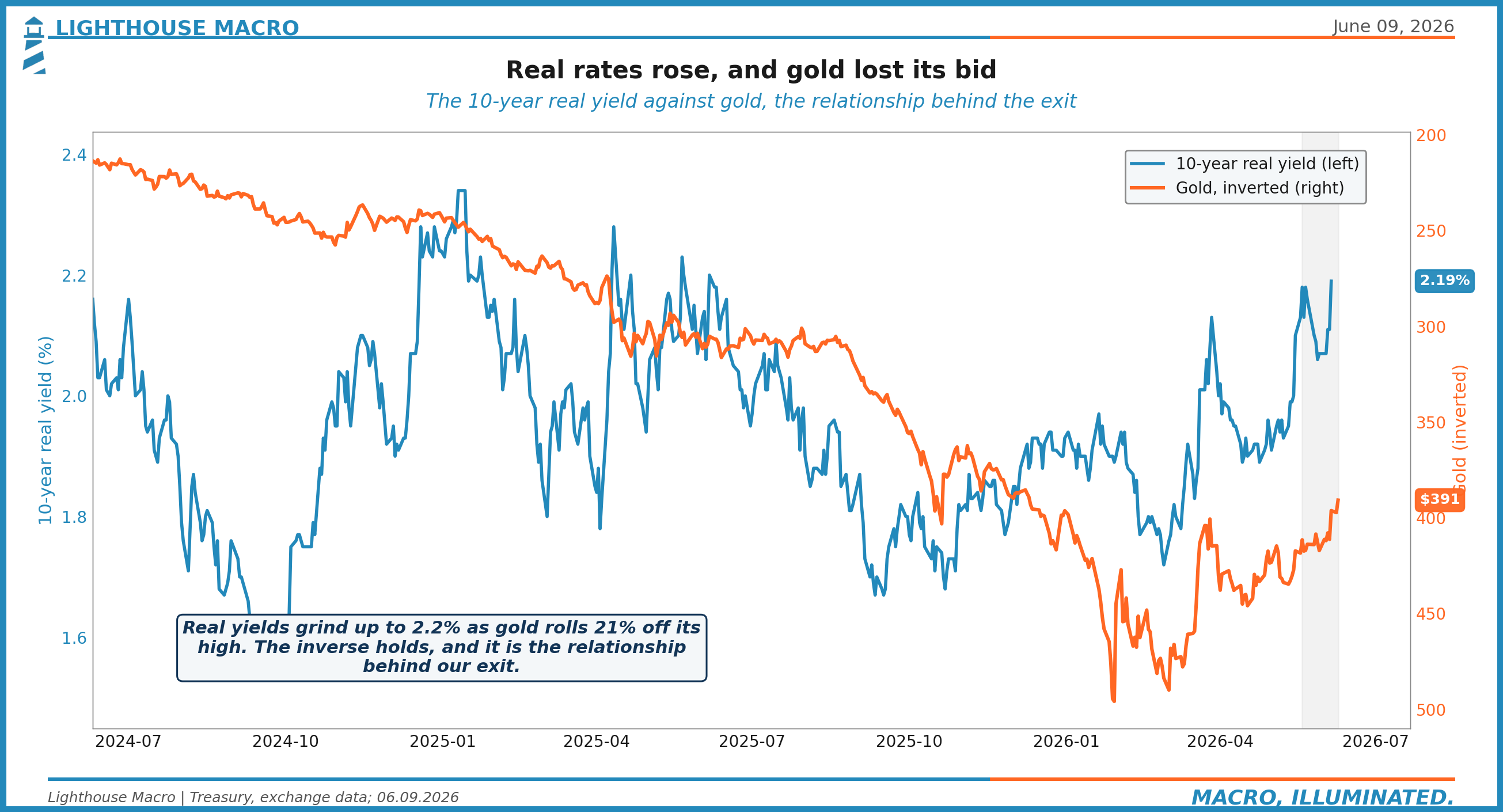

The whole outlook rests on one fact, and here it is plainly. The back-up in yields is real and it is fiscal. Not an inflation print. The real 10-year sits near 2.2%, the high end of its fifteen-year range and still shy of the 2023 peak around 2.5%, while breakevens have behaved and parked near 2.35%. This is a market repricing the price of money for a fiscal reason, term premium and fiscal dominance, the long end demanding to be paid more to hold duration in a world of relentless supply. The 30-year is pushing 5%, and it printed just over it last week.

That distinction is the entire piece. A real-rate regime is a sorting machine, and it sorts without mercy, paying zero-duration cash a real return while it punishes anything long-duration, anything that trades like a bond, anything whose multiple was built on a discount rate that no longer exists. It crushed gold. It carries the long end. And it quietly compresses the multiple on the growth complex that led for two years. Get the cause of the yield move right and everything downstream falls into place. Get it wrong, call it an inflation scare, and you fight the wrong battle into both prints.

The Engine: Term Premium, and a Chair Who Wants More of It

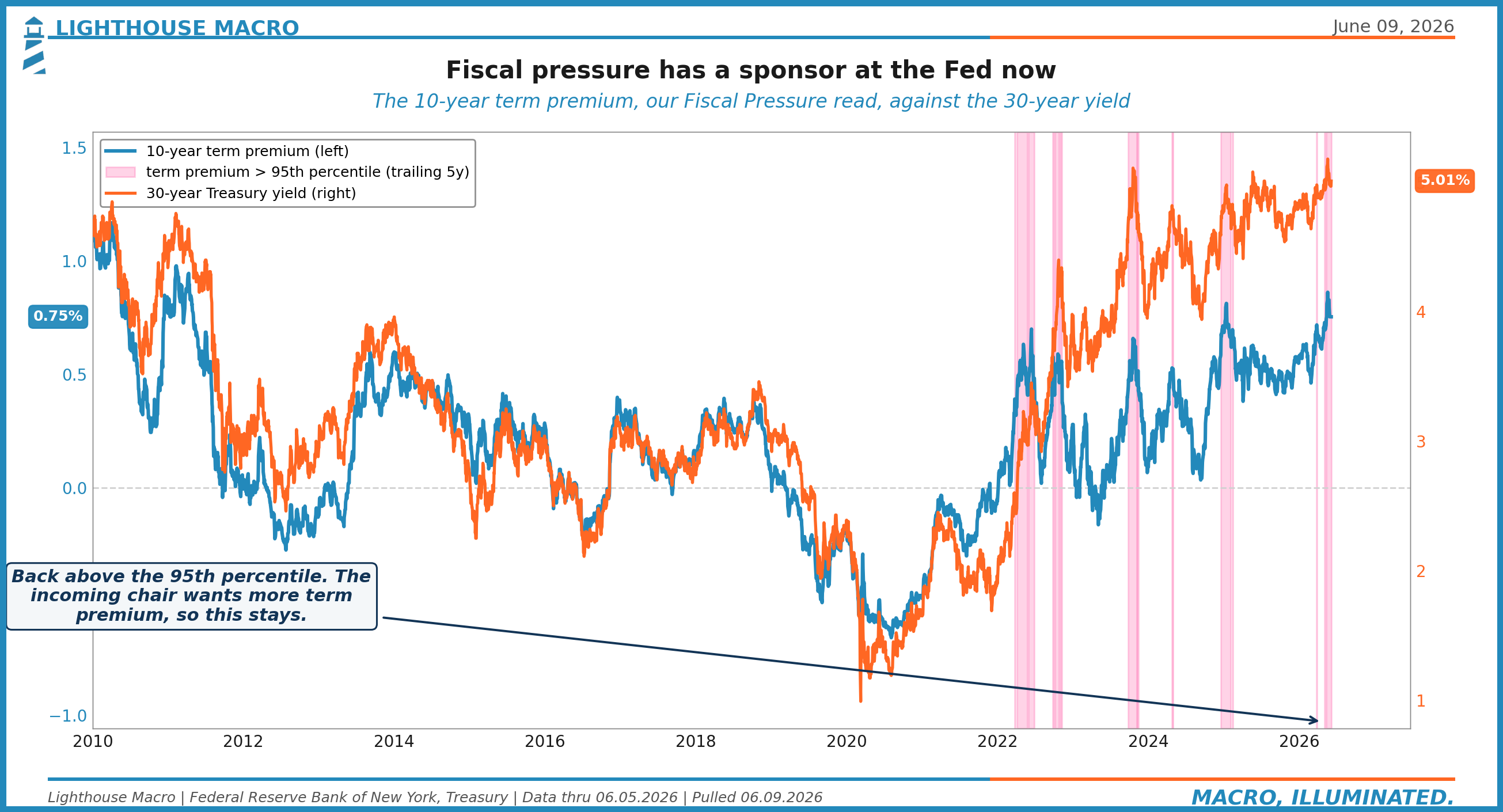

Start with the thing actually moving the long end, because it is also the thing the new Fed chair wants to amplify.

Our Fiscal Pressure read, the 10-year term premium, is back above the 95th percentile of its trailing five-year range. That is the engine pulling the 30-year toward 5%. It is not a forecast of inflation and it is not a growth scare. The bond market is charging rent on duration in a regime of structural deficits and heavy issuance, and that read tells us, as well as anything we track, why the long end refuses to rally even as the front end prices a more restrictive Fed.

Here is what changes the calculus for the next twelve months. The chair is now Kevin Warsh, and June 16-17 is his debut. His agenda is not subtle and it is not new, he has been writing it for years. Sound money. Active balance-sheet shrinkage. The deliberate removal of the easing bias that the prior regime baked into every statement. And, most consequential for the long end, a steeper curve engineered through balance-sheet composition, shifting the Fed’s holdings to push term premium higher rather than suppress it.

Read that against Figure 2 and the implication is stark. The force already driving the 30-year toward 5% is the force the new chair wants to lean into, not against. A Fed that wants more term premium is a Fed that is comfortable with a higher long end, comfortable with a steeper curve, comfortable letting duration reprice. That is a regime that rewards short duration and rate-insensitive defensives and punishes the long-duration growth trade. It runs against the reflex the last fifteen years trained into everyone, the reflex that says the Fed will eventually come to the rescue of the long end. This one might not want to.

The Gap: Laggards Catching Down, Credit Still Asleep

Markets turn in order. They always have. The leading indicators move, the lagging confirmations follow, and the gap between them is where the information lives. Right now the gap is wide and closing.

What the leaders flashed weeks ago has been the same trio the whole way down: breadth thinned, the term premium climbed, and real rates backed up while the index kept printing highs on fewer and fewer names. This week the followers started to catch down. The VIX is on a 20-handle. The spread between QQQ and SPX one-month implied vol hit a four-year high, the options market telling you exactly where it expects the next leg of pain, in the megacap-tech complex that carried the index. Net new 52-week highs sit near 3% on a ten-day average, breadth still narrow even on the bounces. Megacap tech rolled a second leg lower this week after a one-day relief pop. The tape is doing the thing the leaders said it would do.

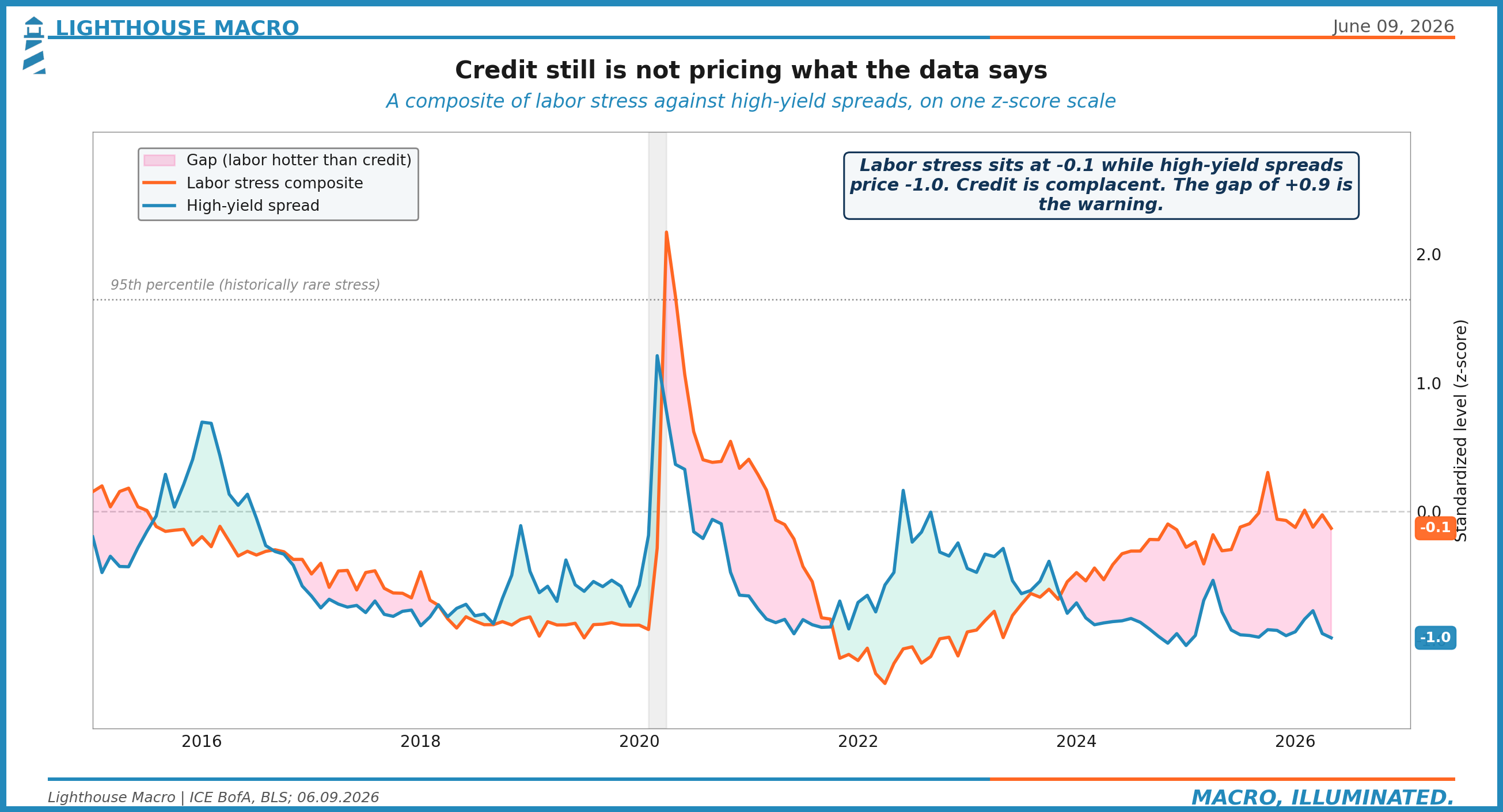

And then there is the one confirmation that has not arrived, the tell at the heart of the whole setup. Public credit spreads are still at the tights. High-yield option-adjusted spread sits near 2.75%, investment grade near 0.75%, both in the record-tight decile. The bond market that is supposed to sniff out stress first is fast asleep.

We do not read that as a refutation. We read it as the lag itself. Cash credit is the last domino, the slowest of the lagging confirmations, and the fact that it has not moved is exactly consistent with a tape that is turning in order with credit at the back of the line. The complacency is loudest in the place that should be most alert.

We want to be precise about what Figure 3 says and does not say. Labor is not stressed. The labor read is neutral, sitting right around its average. The point is that credit is priced tighter than even a neutral labor backdrop warrants. Spreads are pricing perfection, into a regime that is removing the easing bias that perfection was leaning on.

Now look one layer down, because the camouflage matters. Public credit is asleep, but the public number is dominated by a handful of insulated megacap issuers who can fund themselves in any weather. The cracking is happening on the private side, where the marks are slower and the exits are gated. Direct-lending stress, by the data we track, is running above its multi-year norm. Business-development-company redemption gates have reportedly come down as quarterly redemption requests pressed against the caps, which is the polite institutional way of saying the line for the exit got too long. And a rising share of leveraged-loan defaults appears to be running through liability-management exercises, the amend-and-extend machinery that keeps a default from printing as a default and keeps the headline rate looking benign. We flag these as directional reads off the private-credit tape, not pinned, audited figures, because that corner of the market does not mark cleanly or report on time.

That last point is the whole game. The public spread is camouflage. The stress is real, it is just being held in the slowest-marking, least-liquid corner of the credit complex, and the public side mean-reverts to the private, not the other way around. When the gap closes it closes downward, toward where private credit is already telling you the risk sits. Up in quality, short in duration, and no reach for credit here.

The index near its highs on 57% participation is a narrow tape. A few names are doing the work, and the names doing the work are precisely the ones a higher discount rate punishes. That brings us to the internals.